Futures Margin Requirements

Margin is the deposit that lets a small amount of capital control a large futures position — but it works nothing like stock margin. Learn the difference between initial and maintenance margin, how a margin call happens, why futures margin is a performance bond rather than a loan, and how to manage the leverage it creates.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 17 July 2026 · Editorial policy

Before this, read

Introduction

Margin is the mechanism that gives futures their extraordinary power — and their capacity to ruin the careless. It's the reason a trader with £5,000 can control £100,000 of exposure. But the word "margin" causes real confusion, because it means something quite different in futures than it does in shares. In the stock world, margin is a loan. In futures, it's a deposit — a performance bond guaranteeing you can pay your losses.

Getting this right is not pedantry; it changes how the risk works, whether you pay interest, and how quickly a losing trade can spiral. This article explains the two kinds of margin, how a margin call unfolds, why futures margin is not borrowed money, and — most importantly — how to keep leverage from turning an ordinary loss into a catastrophic one.

Quick Definition

Margin in futures is the deposit you post to open and hold a position — a good-faith performance bond, not a loan. Initial margin is what you need to open a trade; maintenance margin is the minimum equity you must keep to hold it. Fall below the latter and you face a margin call.

Initial vs Maintenance Margin

Two thresholds govern every futures position.

- Initial margin is the deposit required to open the position. Set by the exchange and your broker, it's typically 3–12% of the contract's notional value — enough to cover a plausible bad day, not the whole contract.

- Maintenance margin is the equity you must keep in the account to hold the position open. It sits a little below the initial margin. As long as your equity stays above it, you're fine.

The gap between the two lines is your buffer. Trade at the bare minimum and that buffer is thin; a single adverse move can push you into a margin call almost immediately.

The Margin Call

Because futures are marked to market daily (see Futures Settlement), losses are deducted from your account every day. When those losses drag your equity below the maintenance margin, you receive a margin call: a demand to deposit enough funds to restore your account to the initial-margin level.

You have two choices — add money, or reduce/close the position. If you do neither, the broker will liquidate the position for you, often at a poor moment, to protect itself. Margin calls are not a punishment; they're the system's way of ensuring losses are always covered before they become someone else's problem. But they can force you out of a trade at exactly the wrong time, which is why savvy traders keep a healthy buffer well above the maintenance line.

Why Futures Margin Is Not A Loan

This is the distinction that trips up anyone coming from shares. When you buy stock "on margin", you borrow money from your broker to buy more than your cash allows, and you pay interest on that loan.

Futures margin is different in kind. You are not borrowing anything — there's nothing to borrow, because a futures contract isn't bought outright; it's an agreement. Your margin is a performance bond: a deposit held to guarantee you can cover your losses. Consequently:

- You pay no interest on futures margin.

- The margin isn't the "cost" of the contract; it's collateral.

- Your leverage comes from the contract structure itself, not from a loan.

Understanding this clarifies why futures leverage is so high and so cheap — and why the risk lands entirely on price moves rather than borrowing costs.

Day-Trade vs Overnight Margin

Many brokers apply two different margin levels depending on how long you hold:

- Overnight (initial) margin is the full exchange requirement, needed to carry a position through the market close into the next session. It's higher because prices can gap sharply overnight on news, with no chance to react.

- Day-trade (intraday) margin is often much lower, offered by brokers for positions opened and closed within the same session, where the gap risk is absent.

The lower day-trade margin tempts beginners into oversized positions, because it looks like you can afford far more. Resist it: reduced margin means more leverage, not less risk. The contract's true exposure hasn't shrunk at all.

The Leverage Margin Creates

Margin and leverage are two sides of one coin. If a contract worth £100,000 requires £5,000 of margin, you're running 20× leverage — every 1% move in the underlying is a 20% move on your deposit. That's why futures can multiply returns so fast, and why they can erase an account just as fast.

The crucial, sobering fact: because losses are magnified and can exceed your margin, you can lose more than you deposited. A sharp gap against a leveraged position can leave your account negative, meaning you owe the broker. This is the single most important risk to internalise before trading futures with real money.

Managing Margin Risk

The professionals' habits are unglamorous and effective:

- Never trade at maximum leverage. Keep account equity comfortably above the maintenance requirement so ordinary volatility can't trigger a call.

- Size by risk, not by margin. Decide what you're willing to lose on a trade (using your tick value from Contract Specifications), then choose the contract count and size — often a micro contract — to fit.

- Keep a cash buffer. Spare capital in the account absorbs losses without forcing liquidation.

- Respect overnight risk. Don't carry a heavily leveraged position through the close unless you can withstand a gap.

Margin discipline is what separates futures traders who survive from those who don't. The market will hand you leverage freely; using less of it than you're allowed is a feature, not a weakness.

Common Misconceptions

"Margin is the cost of the contract." No — it's a refundable deposit (collateral). You get it back when you close, adjusted for your profit or loss.

"Futures margin works like buying shares on margin." They share a name but not a nature. Stock margin is a loan with interest; futures margin is an interest-free performance bond.

"The most I can lose is my margin." Dangerously false. Leverage means losses can exceed your deposit, leaving you owing the broker. Losses are not capped at your margin.

"Low day-trade margin means it's safer." The opposite — lower margin means higher leverage. The contract's real exposure is unchanged; your cushion is just thinner.

Real-World Application

Suppose the E-mini S&P 500 requires $13,000 initial and $12,000 maintenance margin, and you deposit exactly $13,000 to open one contract. The index promptly falls, and mark-to-market deducts $1,200 that day. Your equity is now $11,800 — below the $12,000 maintenance line. The next morning you get a margin call to restore your account to $13,000: you must wire $1,200, or the position gets closed.

Because you funded the account with the bare minimum, a single ordinary down-day forced a call. Contrast a trader who deposited $20,000 for the same one-contract position. After the same $1,200 loss, their equity is $18,800 — miles above maintenance. They face no call, no forced sale, and can manage the trade on their own terms. Same market, same contract, same loss — but a buffer turned a crisis into a non-event.

Now imagine the fall had been a violent 4% overnight gap: roughly $10,000 against one ES contract. The minimum-funded trader's entire deposit is nearly wiped out and could go negative, leaving them owing money. This is leverage's dark side made concrete — and the reason margin discipline, not margin permission, is what keeps a futures account alive.

Key Takeaways

- Margin in futures is a performance bond, not a loan — you pay no interest, and it's collateral against your losses.

- Initial margin opens a position; maintenance margin is the equity floor to hold it. Falling below triggers a margin call.

- A margin call demands more funds or the broker liquidates your position — often at a bad time.

- Day-trade margin is lower than overnight margin, but lower margin means more leverage, not less risk.

- Because leverage magnifies losses, you can lose more than your deposit — the defining risk of futures.

- Survival comes from margin discipline: never max out leverage, size by risk, and keep a cash buffer.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

Futures Settlement

Related topics

Futures Contract Specifications

Every futures contract is defined by a precise set of specifications — the underlying, contract size, tick size and value, expiry months and settlement type. Learn to read a contract's 'specs', why the multiplier and tick value determine your real exposure, and how mini and micro contracts scale risk to fit your account.

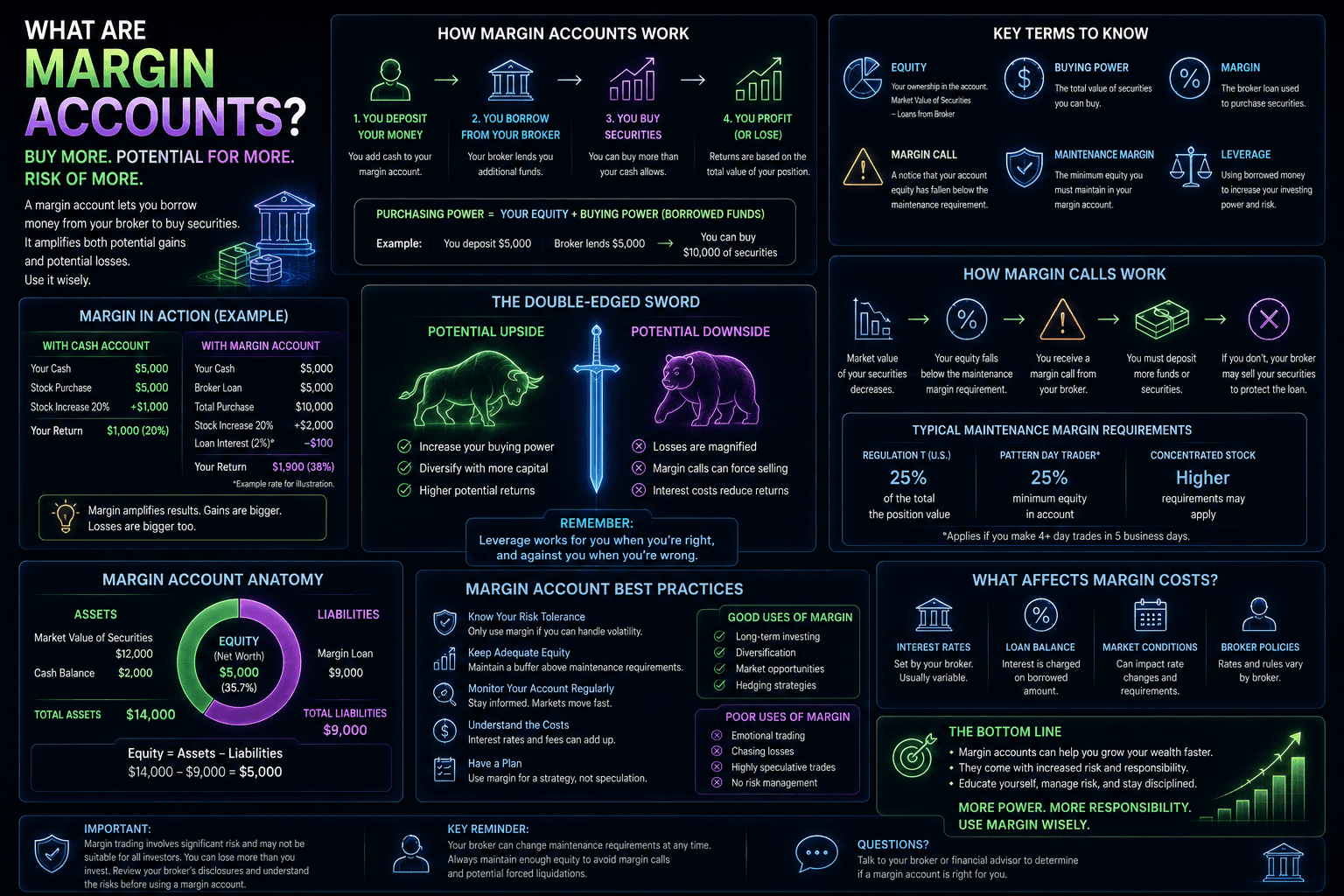

Margin Accounts

Borrowing to invest: how a margin account works, how leverage magnifies gains and losses alike, the mechanics and danger of margin calls and forced liquidation, the cost of margin interest, and why beginners should steer clear.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.