Financial Goals

Why clear goals are the starting point of all investing: how to set them, sort them by time horizon, match each to the right risk and account, and prioritise them through a sensible financial order of operations.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 23 July 2026 · Editorial policy

Before this, read

Introduction

Most people approach investing by asking "what should I buy?" That is the wrong first question. Before any sensible answer is possible, you need to know what the money is for and when you'll need it. A pot for a house deposit in three years and a pot for retirement in thirty are completely different problems, demanding completely different strategies — even for the same person. Financial goals are the starting point of all investing, the compass that points every other decision in the right direction.

This lesson explains why goals come first, how to set them well, how to sort them by time horizon, and how to match each goal to the right level of risk and the right kind of account. It also covers the sensible order of operations — what to do before investing at all — and how to prioritise when, as always, you can't do everything at once. It builds on What Is Investing? and Risk vs Reward, and leads into Building Wealth.

Quick Definition

A financial goal is a specific objective you're saving or investing toward — a defined amount of money needed by a defined time, for a defined purpose.

The three "defined"s matter. "I want to be richer" is a wish, not a goal. "$20,000 for a house deposit in five years" is a goal: it has an amount, a deadline and a purpose, which together make it actionable — you can work out how much to set aside and how much risk you can take. Goals turn vague financial anxiety into a concrete plan.

Why Goals Come First

Investing decisions cascade directly from goals. Consider how much depends on knowing the goal:

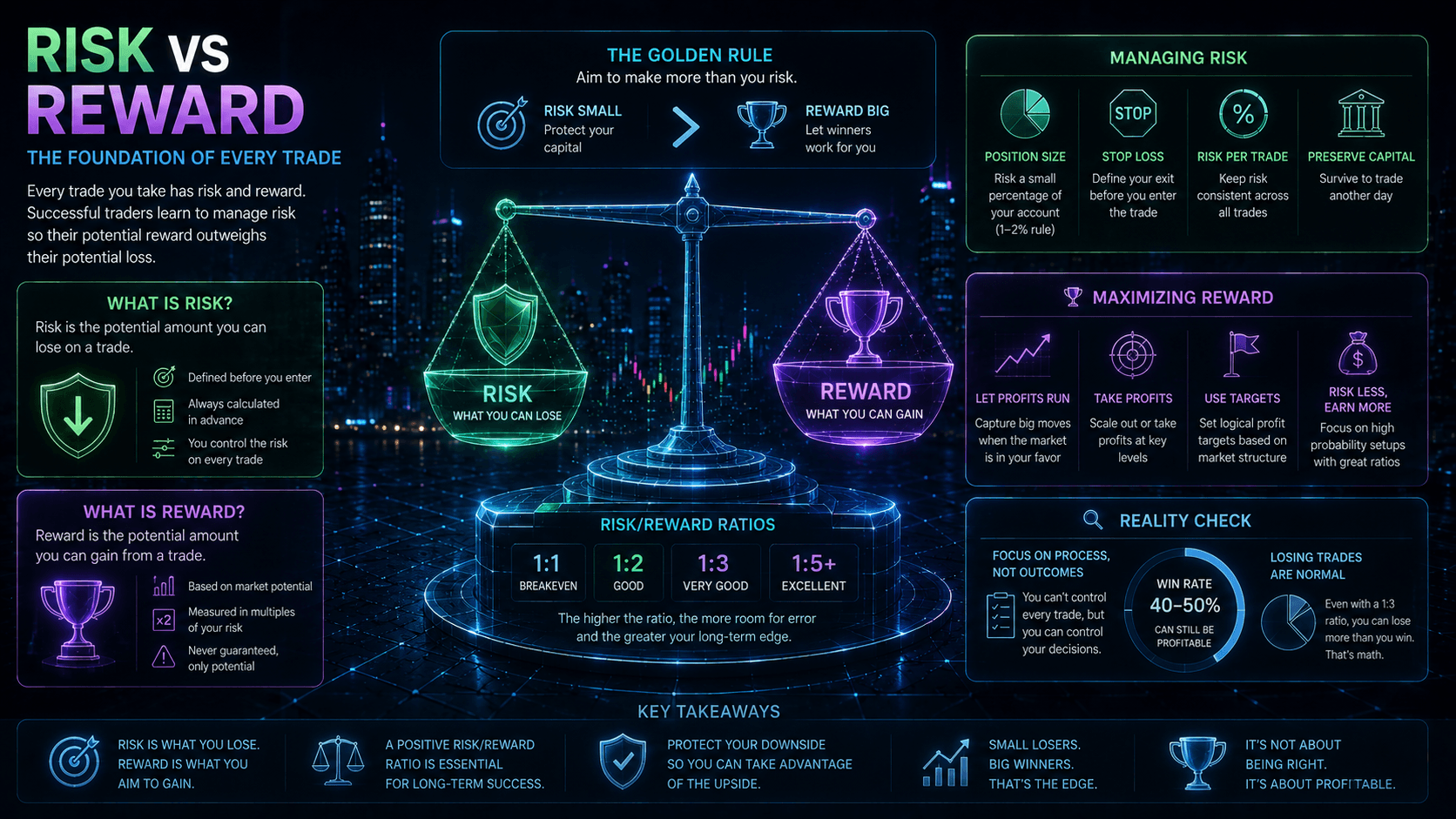

- Time horizon — when you need the money — determines how much risk you can take. (Recall from Risk vs Reward that volatile assets need time to recover.)

- Required amount — combined with your horizon, it tells you how much to save and what return you need.

- Importance — an essential goal (retirement) warrants a different approach from a discretionary one (a luxury holiday).

Without a goal, every investment question becomes unanswerable. Should you buy volatile shares or stable cash? It depends entirely on the goal. Try to invest without one, and you're navigating without a destination — you might move, but you've no way to know if you're heading the right way. This is why thoughtful investors always start here: define the goal, and the right investment strategy largely reveals itself.

Sorting Goals By Time Horizon

The single most useful way to organise goals is by time horizon, because horizon is what links a goal to the right level of risk.

- Short-term goals (0–3 years) — a holiday, a car, a wedding, or your emergency fund. This money can't afford a downturn it has no time to recover from, so it belongs in stable, low-risk holdings like cash or savings, even though they grow slowly. Safety, not growth, is the priority here.

- Medium-term goals (3–10 years) — a house deposit, starting a business. There's some time to ride out volatility, so a balanced mix of growth and stability can be appropriate, dialing down risk as the deadline approaches.

- Long-term goals (10+ years) — retirement, a child's future, financial independence. With a long runway, you can take on more risk to capture the higher expected returns of growth assets like diversified equities, because there's ample time for downturns to recover and compounding to work.

The same person typically has goals in all three buckets at once, each invested differently. This is why "where should I put my money?" has no single answer — it depends which goal the money is for.

Setting Goals Well

A useful goal is specific, measurable and time-bound. Compare "I should save for the future" with "I want $30,000 for a house deposit in 6 years." The second is actionable: dividing the target by the time (adjusting for expected growth) tells you roughly how much to set aside each month, and the 6-year horizon tells you to keep it in moderate-risk holdings. Vague goals can't be planned around; concrete ones can be reverse-engineered into a monthly habit.

It also helps to write goals down and attach a "why." A goal connected to something you genuinely care about — security for your family, freedom to change careers, a comfortable retirement — is one you're far more likely to stick with through the inevitable temptations to spend or the market wobbles that test your resolve. The numbers make a goal actionable; the why makes it durable.

Working backwards: how much to save

Once a goal is specific, you can reverse-engineer it into a monthly habit. Take the target amount, subtract anything you've already saved, and divide by the number of months until the deadline — then adjust for any expected growth on the way. A few illustrative examples:

| Goal | Target | Horizon | Rough monthly saving |

|---|---|---|---|

| Emergency fund | $6,000 | 1 year | ~$500 (in cash) |

| House deposit | $24,000 | 5 years | ~$360 (modest growth) |

| Retirement top-up | $300,000 | 30 years | ~$250 (long-term growth) |

Notice the striking pattern in the last row: a very large long-term goal can need a smaller monthly contribution than a medium one, because decades of compounding do so much of the work (see Compound Growth). This is the practical payoff of pairing goals with horizons — it shows you that even ambitious long-term goals are often achievable with steady, modest saving, while short-term goals simply require setting enough aside because there's no time for growth to help. Working backwards turns an intimidating total into a manageable monthly number.

Common Goals Across Life Stages

While everyone's goals are personal, they tend to follow recognisable patterns across life, which can help you anticipate and plan ahead:

- Early career — building a first emergency fund, clearing student or consumer debt, and starting the retirement habit early (when compounding has the most time to work).

- Establishing years — saving for a home, perhaps a wedding or starting a family, while steadily growing long-term investments.

- Peak earning years — accelerating retirement saving, funding children's education, and paying down a mortgage.

- Approaching and in retirement — shifting long-term pots toward lower risk as the horizon shortens, and drawing down sustainably.

You needn't have all of these, and the order varies, but seeing the typical arc helps you set goals proactively rather than reactively — and reminds you that the early-career habit of starting to invest, even modestly, is disproportionately valuable precisely because it has the longest runway.

The Financial Order Of Operations

Here's a crucial point beginners often miss: investing for long-term goals usually shouldn't be the first thing you do with spare money. There's a sensible order of operations that protects you before you reach for growth.

- Emergency fund first. Build a cushion of roughly 3–6 months' essential expenses in accessible cash. This stops a job loss or surprise bill from forcing you to sell investments at a bad moment or take on debt — it's the foundation everything else rests on.

- Clear high-interest debt. Paying off a credit card charging 20% is effectively a guaranteed 20% return — far better than any investment can reliably offer. Expensive debt compounds against you (see Compound Growth), so clearing it usually beats investing.

- Invest for long-term goals. With a safety net in place and costly debt gone, you can invest for the future with money you won't be forced to withdraw.

- Optimise and expand. Use tax-efficient accounts where available, increase contributions as income grows, and add further goals.

This order isn't rigid dogma, but it captures a sound principle: secure your foundation before reaching for growth. Investing while one credit-card debt quietly compounds at 20% is like bailing water into a leaking boat.

Prioritising And Trading Off

Few people can fund every goal at once, so prioritisation is part of the craft. Essential goals (security, retirement) generally come before discretionary ones (luxuries). Time-sensitive goals may need attention before distant ones. And there are genuine trade-offs: money directed at a near-term holiday is money not compounding for retirement, and vice versa. There's no perfect formula — the point is to make these trade-offs consciously, in line with your values, rather than letting money drift without direction. Even modest progress on several goals at once, deliberately chosen, beats a vague intention to "save more someday."

Needs, Wants And Wishes

When prioritising, a simple three-tier sort cuts through the difficulty. Needs are non-negotiable foundations: an emergency fund, freedom from high-interest debt, and enough retirement provision to avoid hardship later. Wants are important but flexible: a home, a comfortable (not just adequate) retirement, your children's education. Wishes are the discretionary extras: a second home, early retirement, luxury travel.

The principle is to fund needs first and most reliably, wants next, and wishes only with what remains — and to be honest about which is which. Much financial stress comes from funding wishes while needs go unmet, or from treating a want as a need and over-committing to it. This isn't about denying yourself enjoyment; it's about sequencing, so that the foundations are secure before the luxuries, and so that a setback threatens a wish rather than your security. Naming each goal as a need, want or wish makes the inevitable trade-offs far clearer.

Automate It: Pay Yourself First

A goal is only as good as the habit behind it, and the most reliable habit is automation. Rather than saving whatever happens to be left at the end of the month — which is usually little — set up automatic transfers toward each goal as soon as you're paid. This "pay yourself first" approach treats saving like a fixed bill rather than an afterthought, and it removes the monthly decision (and temptation) entirely.

Automation works because it harnesses inertia in your favour: once set up, the right thing happens by default, and you adjust your spending to what remains. It also smooths investing through ups and downs — by contributing the same amount regularly, you buy more when prices are low and less when they're high, without having to time anything. For most people, automating contributions toward clearly defined goals is the single most effective practical step between having a plan and achieving it. The goal sets the destination; automation does the driving.

Reviewing And Adjusting

Goals are not set in stone. Life changes — income rises or falls, families grow, priorities shift, timelines move — and your plan should change with it. A useful habit is to review your goals periodically, perhaps once a year: Are the targets still right? Has a horizon shortened (bringing a goal's money into a lower-risk bucket)? Have you fallen behind or pulled ahead? This isn't about constant tinkering with investments — that often backfires — but about keeping the goals and the strategy matched to them aligned with your real life. A plan you revisit occasionally and adjust thoughtfully is far more likely to succeed than one set once and forgotten.

Common Misconceptions

- "I should pick great investments first, then figure out goals." Backwards — the goal determines which investments are even appropriate.

- "Goals are only for people with lots of money." Goals matter more when money is tight, because they direct limited resources where they count.

- "I should invest every spare dollar immediately." Not before an emergency fund and clearing high-interest debt — the order of operations protects you.

- "Once I set a goal, it's fixed." Goals should evolve with your life; periodic review keeps them realistic and relevant.

Real-World Application

Imagine someone with $500 a month of spare income and three goals: a $6,000 emergency fund, a $4,000 credit-card balance at 22%, and a comfortable retirement in 35 years. The order-of-operations lens gives a clear plan rather than paralysis. First, they build the emergency fund (and clear the card — a guaranteed 22% "return" no investment can match), perhaps splitting effort between the two. Only then do they direct that $500 toward a diversified, long-term retirement portfolio, where decades of compounding can work. Each goal is matched to the right vehicle: cash for the emergency fund, debt repayment for the card, growth assets for retirement. The same $500, directed by clear goals in a sensible order, accomplishes far more than it would scattered without a plan. That is what financial goals do — they turn limited money into deliberate progress.

Key Takeaways

- Financial goals come first — they define the horizon and risk that determine the right investments.

- Sort goals by time horizon: short-term needs safety (cash), long-term can take more risk (growth assets), medium-term sits between.

- Make goals specific, measurable and time-bound, and attach a "why" so you stick with them.

- Follow a sensible order of operations: emergency fund → clear high-interest debt → invest for goals → optimise.

- Prioritise consciously among competing goals, and review periodically as life changes.

- The right investment is always the one that fits the goal — there is no single answer divorced from purpose.

Finished this lesson? Track your progress.

Frequently asked questions

What makes a financial goal different from just wanting to be richer?

A financial goal must have three defined elements: a specific amount of money, a specific deadline, and a specific purpose. For example, "$20,000 for a house deposit in five years" is a goal because it's actionable—you can calculate how much to save monthly and what risk level is appropriate. "I want to be richer" is a wish, not a goal, because it lacks these concrete details.

Why does the time horizon of a goal matter for deciding how to invest?

Time horizon determines how much risk you can afford to take. Short-term goals (0–3 years) need safe, low-risk holdings because there's no time to recover from a downturn. Long-term goals (10+ years) can tolerate higher-risk growth assets because there's ample time for downturns to recover and compounding to work. This is why the same person's different goals require completely different investment strategies.

What types of investments match different goal time horizons?

Short-term goals (0–3 years) should use cash or savings accounts; medium-term goals (3–10 years) suit balanced mixes of growth and stability; long-term goals (10+ years) can use growth assets like diversified equities. The shorter your deadline, the safer your money must be.

How do you calculate how much to save each month for a specific goal?

Take your target amount, subtract what you've already saved, and divide by the number of months until your deadline. Then adjust upward for any expected growth on the money. For example, saving $24,000 in five years requires roughly $360 per month (accounting for modest growth), while a $300,000 retirement goal over 30 years might need only ~$250 monthly because decades of compounding do much of the work.

Why should you write down your financial goals and explain your reasons for them?

Writing goals down and attaching a personal "why"—connecting them to something you genuinely care about like family security or career freedom—makes them durable. While the numbers make a goal actionable and measurable, the emotional connection makes you far more likely to stick with it through spending temptations and market volatility.

Key terms

Next lesson

Continue learning

Building Wealth

Related topics

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.