Investing vs Trading

A head-to-head comparison of investing and trading: how their time horizons, sources of return, costs, effort, risk and psychology differ — and a clear framework for deciding which suits you, or how to combine them safely.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 23 July 2026 · Editorial policy

Before this, read

Introduction

"Investing" and "trading" are often used interchangeably, as if they were the same activity. They are not. They share a marketplace and the same basic mechanics — buying and selling assets — but in almost every way that matters, they are different disciplines, suited to different goals, temperaments and time horizons. Confusing the two is one of the most common and costly mistakes a newcomer can make.

You have already met each on its own terms in What Is Investing? and What Is Trading?. This lesson puts them side by side. We will compare them across the dimensions that actually determine outcomes — horizon, source of return, costs, effort, risk and psychology — and then give you a practical framework for deciding which suits you, and how to combine them safely if you choose to. By the end, the goal is not to crown one "better" in the abstract, but to help you match the right approach to your situation.

Quick Definition

Investing is committing money to productive assets for the long term to capture their growth, income and compounding. Trading is buying and selling more frequently to profit from shorter-term price movements.

They are best understood not as rivals but as different tools for different jobs. A long-term retirement pot and a small, high-risk speculative bet are different problems, and investing and trading are the respective tools. The mistake is using the wrong tool for the job — treating retirement money like a trading account, or expecting trading to deliver the steady, compounding reliability of long-term investing.

What they have in common

Before the differences, it is worth being clear about the genuine common ground, because it is what causes the confusion. Both investing and trading involve buying and selling the same kinds of assets — shares, ETFs, and so on — through the same brokers and the same markets. Both require capital you can put at risk, both involve the possibility of loss, and both reward (in different measures) knowledge, discipline and emotional control. Neither is gambling when done well, and both are forms of speculation in the broad sense that the future is uncertain. Someone watching over your shoulder might struggle to tell an investor placing a trade from a trader placing one — the click looks identical. The differences are not in the mechanics of the transaction but in the intent, horizon and strategy behind it, and in the source of any profit. That shared surface is exactly why so many people drift from one into the other without realising they have changed games — often drifting from the reliable activity into the difficult one.

The Core Difference

Strip away the detail and two linked differences explain everything else: time horizon and source of return.

An investor's time horizon is years to decades, and their return comes from the underlying assets growing in value, paying income, and compounding — the economy doing its work over time. They are, in effect, riding a long-term upward tide that has historically lifted diversified portfolios despite many setbacks along the way.

A trader's horizon is seconds to weeks, and their return comes from correctly anticipating short-term price moves — the choppy waves on top of the tide — repeatedly, after costs. This is a fundamentally different and harder source of return: instead of being carried by growth, the trader must actively out-compete others again and again. The tide rewards patience; the waves reward skill, speed and discipline, and punish their absence.

Side By Side

It helps to see the contrast across every dimension at once:

| Dimension | Investing | Trading |

|---|---|---|

| Time horizon | Years to decades | Seconds to weeks |

| Source of return | Asset growth, income, compounding | Short-term price movements |

| Activity level | Low (buy and hold) | High (frequent) |

| Skill required | Modest (mostly temperament) | High and specialised |

| Time commitment | Minimal | Substantial |

| Costs & taxes | Low (infrequent) | High (frequent) |

| Typical outcome | Tracks market growth over time | Most underperform after costs |

| Main risk | Market falls (recoverable over time) | Losses, costs, behavioural error |

| Emotional demand | Low if diversified | Very high |

No single row settles the matter, but the pattern is unmistakable: investing asks less of you and offers a more reliable path, while trading asks far more and offers a far less certain reward. This is why, for most people most of the time, investing is the sensible foundation and trading is, at best, a small specialist activity.

Notice how the rows reinforce one another rather than standing alone. Trading's short horizon forces high activity, which causes high costs and taxes, which raises the skill bar needed to net a profit, which demands more time and emotional control — a chain in which each disadvantage compounds the next. Investing's long horizon does the reverse: low activity keeps costs and taxes low, which means even an average, patient approach captures most of the market's return, with little time and modest stress. The comparison is not a list of independent trade-offs where trading wins some and investing wins others; it is a coherent picture in which investing's advantages mostly stem from a single virtue — patience — and trading's disadvantages mostly stem from a single demand — constant, skilled activity against tough competition.

Source Of Return: Tide vs Skill

The single most important difference is worth dwelling on. When you invest in a diversified basket of productive assets, you are betting that human enterprise — companies innovating, producing and growing — will create value over time. History strongly supports that bet over long horizons: the tide has risen. You do not need to be smarter than anyone; you need to be patient and stay invested.

When you trade, there is no tide to carry you over minutes or days — prices in the short term are close to a zero-sum contest among participants, and once costs are subtracted, the average trader is in a negative-sum game. To win, you must be genuinely better than the people on the other side of your trades, consistently, by enough to overcome costs. That is possible for a skilled few, but it is the opposite of the "anyone can succeed with patience" promise of long-term investing. Understanding this asymmetry — reliable tide versus hard-won skill — is the heart of the comparison.

Costs, Taxes And Effort

Three practical differences reinforce the picture:

- Costs. Every trade crosses a spread and may incur fees. An investor making a handful of transactions a year barely notices; a trader making many a week faces a large, recurring drag that their skill must overcome before they make a penny.

- Taxes. In many jurisdictions, short-term gains are taxed more heavily than long-term ones, and frequent trading realises taxable gains constantly, whereas a buy-and-hold investor can defer tax for years and let the full amount compound.

- Effort. Sound investing can take a few hours a year — choose a diversified, low-cost approach, automate contributions, rebalance occasionally. Trading can be a full-time job demanding constant attention, analysis and emotional management. The return on time invested is, for most people, vastly higher with investing.

To make the costs concrete, imagine two people who each earn the same 8% gross return on $10,000 over a year. The investor makes three trades all year, paying perhaps $15 total in costs and deferring tax — they keep almost the entire 8%. The trader churns the account, paying spreads and fees on dozens of trades that add up to, say, 6% of the account, and realising short-term taxable gains taxed at a higher rate. Same gross return, wildly different net outcome: the investor pockets close to $800, while the trader, after costs and tax, might keep a fraction of that — and that is in a year where the trader actually matched the market, which most do not. The lesson is stark: in trading you can be right and still lose to your own costs, whereas investing lets the full return compound largely untouched.

Psychology And Temperament

The two approaches also demand very different temperaments. Investing rewards the ability to do nothing — to stay calm through downturns, ignore the noise, and let compounding work. Its hardest moments are emotional: not panic-selling when markets fall.

Trading rewards a rarer and more intense psychological profile: the ability to make rapid decisions under pressure, cut losses without ego, avoid chasing, and execute a plan mechanically while real money swings around. The short time frame amplifies fear and greed, and most people — however intelligent — find that their emotions sabotage their results. Honestly assessing your own temperament is as important as any analysis: many people who would make excellent patient investors make poor, stressed traders.

Where The Line Blurs

The distinction is clear at the extremes — a thirty-year index holding versus a thirty-second scalp — but there is a genuine grey zone in the middle, and being honest about it prevents confusion. A position trader holding a trend for several months looks a lot like a short-term investor. Someone who buys an individual company they believe in, intending to hold for a year or two based on its prospects, is arguably doing a bit of both. And an investor who occasionally rebalances or adjusts their holdings is making active decisions without becoming a "trader."

The useful test is not the time held alone but the source of expected return and the basis of the decision. If you are buying because you expect the underlying asset to grow in value over a meaningful period — and you would be comfortable holding through volatility — you are investing, even if you sometimes sell. If you are buying because you expect the price to move in your favour soon, intending to sell on that move regardless of the asset's long-term merit, you are trading, even if "soon" means a few months. Naming which game you are playing on each decision keeps you honest, because the danger is sliding from a patient investment thesis into anxious price-watching without noticing — turning a sound long-term holding into a stressful short-term bet.

The Rise Of Retail Trading

It is worth understanding why this comparison matters more now than ever. A decade or two ago, trading was costly and cumbersome enough that most ordinary people simply invested by default. Today, commission-free apps, fractional shares, and slick mobile interfaces have put fast, frequent trading in everyone's pocket — and an enormous online culture actively promotes it, often making trading look both easy and lucrative.

This democratisation has real benefits: investing has never been more accessible. But the same forces have blurred the line and nudged millions of new participants toward the harder of the two activities, frequently without understanding the odds. Gamified design — streaks, notifications, celebratory animations on trades — can turn what should be patient investing into compulsive trading. Recognising this environment for what it is helps you resist it: the platform's incentive is often to maximise your activity, while your interest is usually served by less of it. Choosing investing over trading is, in part, choosing to opt out of a system designed to make you trade more than is good for you.

Which Is Right For You?

The choice should flow from your goals, your available time, and your temperament — not from which sounds more exciting.

For the overwhelming majority of people — anyone building toward retirement, a home, or financial security with limited spare time — long-term investing is the right foundation, often the whole answer. Trading enters the picture only for those with genuinely spare money they can afford to lose, spare time to develop real skill, and a clear-eyed acceptance of the high probability of loss. Even then, it should be a small part of the whole.

Can You Do Both?

Yes — and if you want exposure to trading, the responsible way to combine them is a core-satellite approach.

In this structure, the core — the large majority of your money — sits in long-term, diversified investments doing the patient work of compounding. A small satellite — money you have explicitly decided you can afford to lose — is set aside for trading or higher-risk bets. This lets you scratch the trading itch, learn, and pursue potential outperformance without jeopardising the foundation of your financial future. The cardinal rule is that the satellite must never cannibalise the core: a bad trading run should be disappointing, not life-altering.

Common Misconceptions

- "Trading is just faster investing." They have different sources of return; trading is not a sped-up version of the same reliable process.

- "Investing is for the timid; trading is for the ambitious." Ambition is better served by the approach that actually builds wealth for most people — patient investing — than by an activity most people lose at.

- "You must choose one or the other." You can do both via core-satellite, as long as the trading portion is small and ring-fenced.

- "Trading will make me rich faster." Occasionally for a skilled few; for most, it erodes wealth faster than patient investing builds it.

Real-World Application

Consider someone in their thirties with $20,000 and a stable income who wants both long-term security and an interest in markets. The sound approach is clear: put the bulk — say $19,000 — into a diversified, low-cost long-term investment portfolio aligned to their retirement and goals, and leave it largely alone to compound for decades. If they genuinely want to trade, they ring-fence a small satellite — perhaps $1,000 they can afford to lose entirely — to learn with, fully aware most of it may evaporate. Years later, the core has quietly done the heavy lifting of building their wealth, while the satellite scratched the itch and taught some lessons, for better or worse. This is investing and trading in their proper proportions — the foundation built on the reliable tide, with only a small sail set to catch the waves.

Key Takeaways

- Investing and trading share a market but differ in horizon and source of return — the tide of long-term growth versus the waves of short-term price moves.

- Investing is lower-cost, lower-effort, lower-stress and carried by growth; trading is costly, demanding and competitive, and most people lose at it after costs.

- The right choice flows from your goals, time and temperament — for most, long-term investing is the foundation.

- If you want to trade, use a core-satellite approach: a large long-term core and a small, ring-fenced trading satellite.

- Never let the satellite cannibalise the core — your financial future should rest on the reliable tide, not the waves.

Finished this lesson? Track your progress.

Frequently asked questions

What is the main difference between investing and trading?

Investing commits money to assets for the long term (years to decades) to capture growth, income and compounding from the underlying assets. Trading buys and sells more frequently (seconds to weeks) to profit from short-term price movements. The key difference is that investors ride the long-term upward tide of economic growth, while traders try to profit from the choppy waves on top of that tide.

Why does trading have higher costs than investing?

Trading requires frequent buying and selling, which generates transaction costs and taxes with each trade, while investing's buy-and-hold approach means infrequent activity and minimal costs. Trading's short time horizon forces high activity, and each trade triggers costs that compound the difficulty of achieving net profits after expenses.

What skills are needed for investing versus trading?

Investing requires mostly modest temperament and patience — the ability to hold through market downturns and let compounding work over time. Trading requires high, specialised skill because the trader must repeatedly and correctly anticipate short-term price movements while competing against others, all while managing higher emotional demands and costs.

Why do most traders underperform while most investors succeed?

Investing's long time horizon keeps costs and activity low, allowing even an average, patient approach to capture most of the market's reliable growth. Trading's short horizon forces frequent activity, high costs and taxes that raise the skill bar to an extremely high level — most traders cannot overcome these disadvantages to beat the market after costs.

Can someone do both investing and trading at the same time?

Yes, investing and trading are different tools for different jobs — a long-term retirement account and a small speculative account serve different purposes. The key mistake is using the wrong tool for the job, such as treating retirement money like a trading account or expecting trading to deliver the steady reliability of long-term investing.

Key terms

Next lesson

Continue learning

Risk vs Reward

Related topics

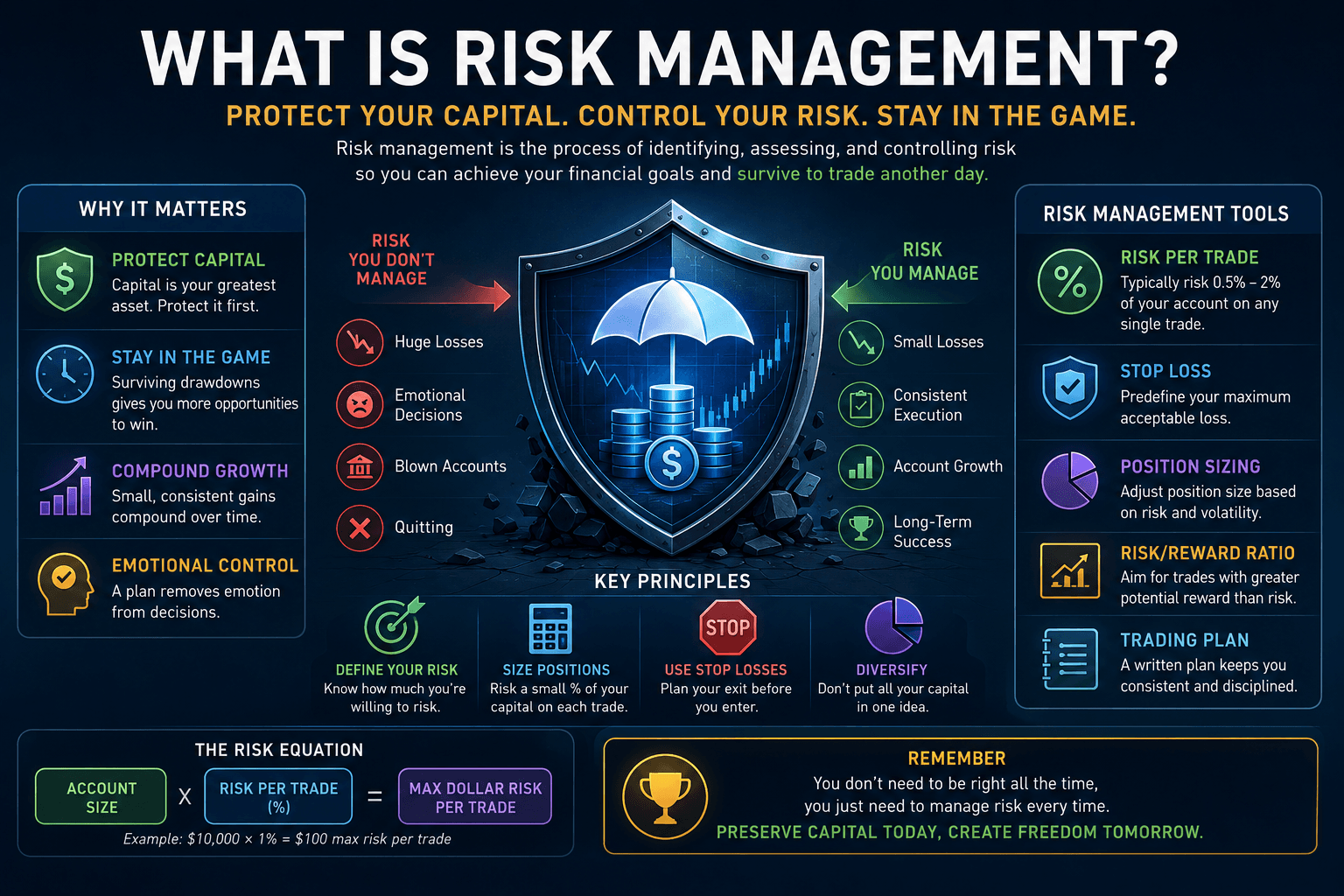

What Is Risk Management?

A practical guide to the discipline that protects investors: why avoiding ruin matters more than maximising gains, the brutal maths of large losses, position sizing, diversification, drawdowns, and matching risk to your goals.

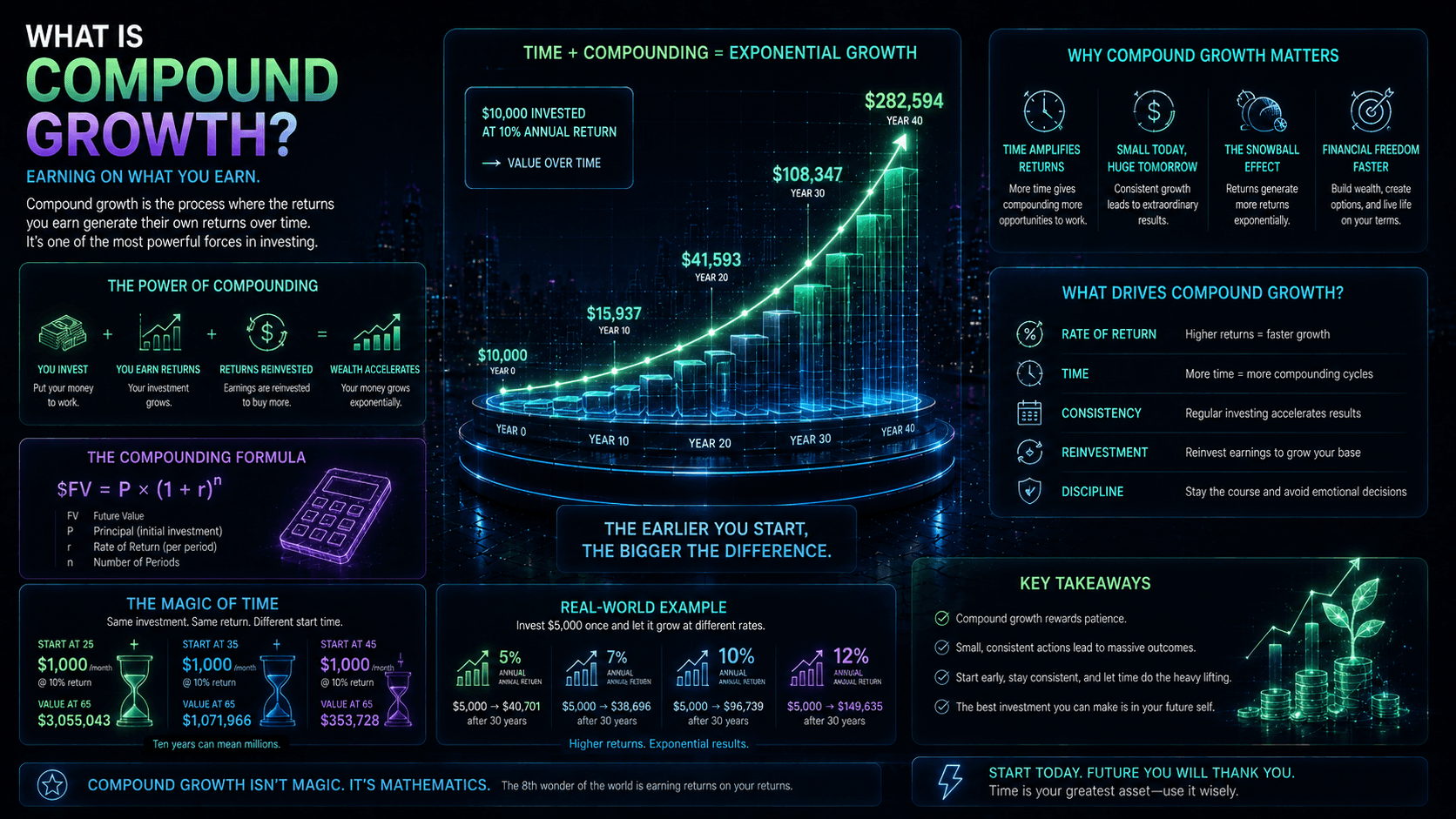

Compound Growth

The most powerful force in investing: how returns earning returns turns modest sums into large ones over time, the three levers that drive it, why starting early matters most, and how compounding can work against you too.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.