What Is Wealth Building?

Wealth building isn't about picking hot stocks or getting lucky — it's a slow, boring, almost mechanical process of spending less than you earn, investing the difference, and letting time and compounding do the heavy lifting. Learn the real levers of wealth, why behaviour matters more than brilliance, and the mindset that builds lasting security.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 17 July 2026 · Editorial policy

Before this, read

Introduction

There's a myth that building wealth requires a special talent — an eye for the next big stock, insider knowledge, or a lucky break. The truth is far more encouraging and far more boring: wealth building is a process, not a talent. It's the almost mechanical result of spending less than you earn, investing the difference, and giving it enough time. Anyone who does this consistently, and avoids a few big mistakes, can build real, lasting wealth — no genius required.

This is the opening article of the Retirement & Wealth Building category, and its job is to reframe how you think about money over a lifetime. The strategies that follow — pensions, tax wrappers, drawdown, FIRE — are all tools in service of this one simple, powerful idea. Get the mindset right, and the tools do their work.

Quick Definition

Wealth building is the long-term process of consistently spending less than you earn, investing the surplus sensibly, and letting time and compounding grow it into lasting financial security.

The Wealth-Building Equation

At its heart, building wealth comes down to a simple chain:

Earn → keep a surplus (spend less than you earn) → invest the surplus → let it compound over time

Each link matters. You need income, but income alone isn't wealth — plenty of high earners have little, because they spend it all. You need a surplus, the gap between what you earn and what you spend, because that gap is the only thing you can actually invest. You need to invest it (not leave it in cash, which inflation erodes) so it grows. And above all you need time, because compounding — the engine that turns modest sums into large ones — only works over long horizons.

Time Is Your Greatest Asset

Of all these levers, time does the most work, because compounding is exponential. Money invested early has the longest to multiply, so the earliest pounds you invest are worth far more to your final wealth than pounds invested later.

This is why the single most valuable piece of wealth-building advice is simply start now. Not when you earn more, not when markets look calm — now, with whatever you can. The years you spend invested are working for you in a way no later effort can replace.

Behaviour Beats Brilliance

Here's the finding that surprises people: over a lifetime, how you behave matters more than what you pick. The investor who calmly saves every month and stays invested through every crash will, in most cases, end up wealthier than the one who chases clever strategies but panics in downturns or forgets to keep contributing.

The behavioural traps are the real enemies of wealth: not saving consistently, panic-selling in crashes (turning temporary losses permanent — see Loss Aversion), chasing hot trends, and paying high fees that quietly erode returns for decades (see The Impact of Fees). Avoid these, and you've done more for your wealth than any amount of clever selection. Wealth building is won by discipline and defence, not by dazzling offence.

Why It's Meant To Be Boring

Reliable wealth building is deeply unexciting, and that's a feature, not a bug. It looks like: automate a monthly contribution, invest it in something broad and cheap, ignore the news, and repeat for decades. There are no thrilling wins because there are no thrilling risks. The "exciting" alternatives — hot tips, day trading, the next big thing — almost always carry the higher risk that destroys wealth rather than builds it.

If your wealth-building plan feels boring, you're probably doing it right. The excitement in personal finance is usually the sound of money being lost.

Common Misconceptions

"I need to earn a lot to build wealth." Income helps, but the gap between earning and spending is what you invest. Modest earners who save consistently often outbuild high earners who spend it all.

"I'll start investing when I have more money." The cost of waiting is enormous, because you lose the most valuable years of compounding. Starting small now beats starting big later.

"Building wealth means finding great investments." It mostly means great habits — saving, staying invested, keeping costs low, and not panicking. Selection matters far less than behaviour over time.

"It's too late for me to start." The best time was years ago; the second best is today. Even a shorter runway benefits from compounding, and every year invested helps.

Real-World Application

Consider two people. Priya starts at 25, investing £200 a month into a cheap global fund, and simply keeps going — through crashes, through booms, never stopping, never chasing. She doesn't earn a fortune and she never picks a single individual stock. Ben starts at 40, earning much more and investing £500 a month, but he tinkers constantly, sells in a panic during one bad crash, and pays for expensive "expert" funds. Despite investing more money each month, Ben may well end up with less than Priya by retirement — because Priya had fifteen extra years of compounding, stayed invested through the storms, and kept her costs and mistakes low.

The difference wasn't income, intelligence or stock-picking. It was time and behaviour — starting early and staying the course. That is the entire secret of wealth building, and it's available to almost anyone willing to be patient and consistent. The rest of this category simply shows you the best tools — pensions, ISAs, tax efficiency — to make Priya's boring, powerful process as effective as possible.

Key Takeaways

- Wealth building is a process: spend less than you earn, invest the surplus, and let time compound it — consistency, not talent.

- The core levers are earn more, spend less, invest wisely, and give it time — and time does the most work.

- Starting early is disproportionately powerful because compounding is exponential; the earliest pounds grow the most.

- Behaviour beats brilliance: saving steadily, staying invested through crashes, and keeping costs low matter more than what you pick.

- Good wealth building is deliberately boring — excitement usually signals risk that destroys wealth rather than builds it.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

Time in the Market vs Timing the Market

Related topics

Pound-Cost Averaging

Pound-cost averaging means investing a fixed amount at regular intervals, whatever the market is doing. Learn how it automatically buys more when prices are low and less when high, why it removes the stress and risk of timing, how it compares with investing a lump sum, and why it's the natural engine of wealth building.

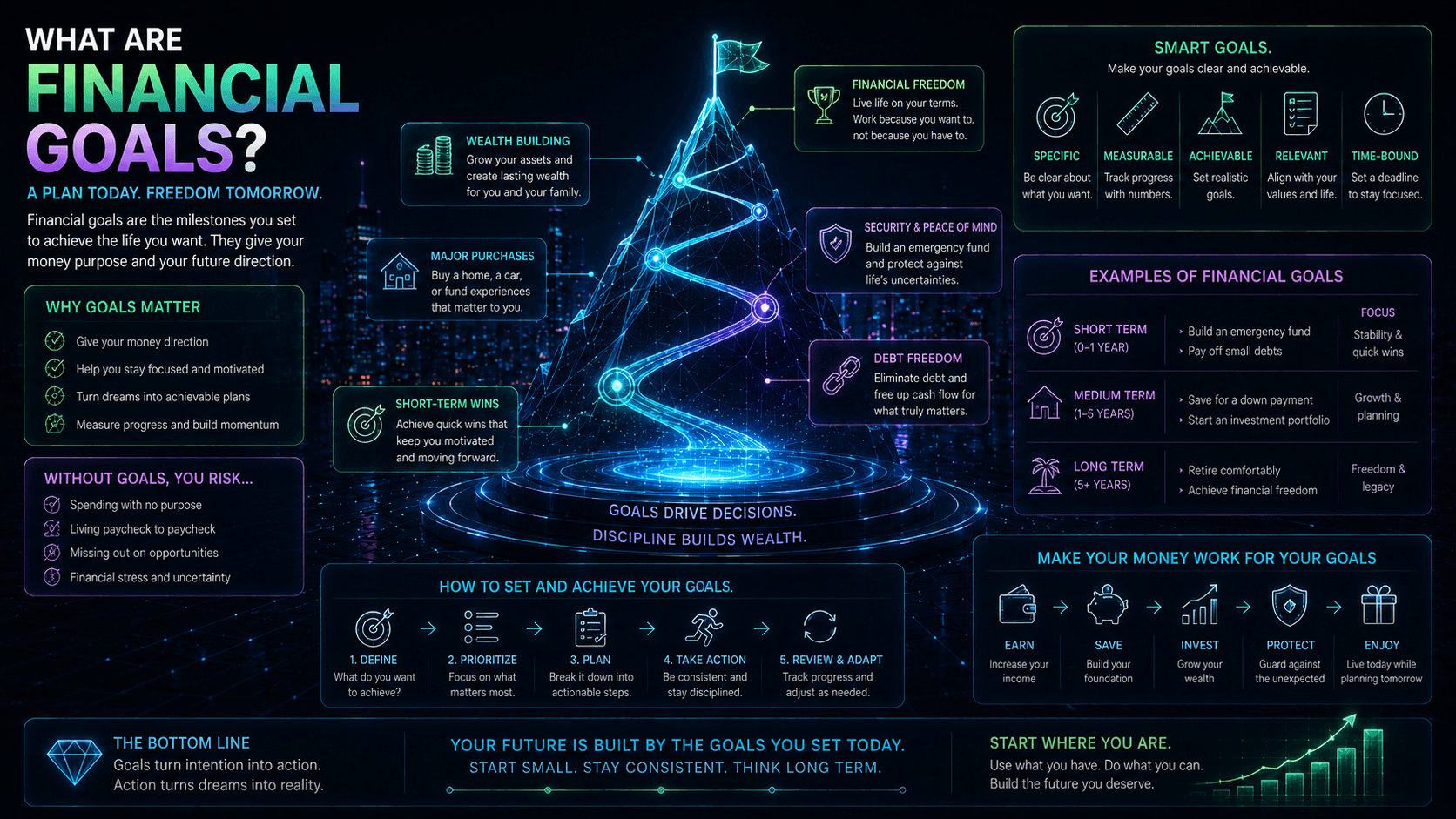

Financial Goals

Why clear goals are the starting point of all investing: how to set them, sort them by time horizon, match each to the right risk and account, and prioritise them through a sensible financial order of operations.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.