Retirement Accounts

The big picture of saving for retirement: why tax-advantaged retirement accounts exist, the three pillars (state, workplace and private pensions), why an employer match is free money to claim first, and the priority order for your contributions.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 23 July 2026 · Editorial policy

Before this, read

Introduction

Retirement can feel impossibly distant, especially when you're young — but it is the single largest financial goal most people will ever fund, and the one where starting early matters most. The tools built to help are retirement accounts: tax-advantaged pensions designed specifically to encourage and reward long-term saving for later life. Understanding how they fit together is one of the most valuable pieces of financial knowledge you can acquire.

This lesson takes the big-picture view. Rather than the mechanics of one account, it explains why retirement accounts are tax-advantaged, the three pillars that typically make up retirement income, why an employer match is "free money" you should claim first, and the sensible priority order for your contributions. It builds on What Is Investing? and ties together the specifics covered in ISAs and SIPPs. (Rules are UK-focused and can change; this is education, not advice.)

Quick Definition

Retirement accounts are tax-advantaged accounts — chiefly pensions — designed to help you save and invest for later life. In exchange for tax benefits, they typically restrict access until a minimum age, encouraging the money to stay invested for the long term.

The defining bargain of a retirement account is tax incentives in exchange for patience. Governments want people to provide for their own retirement, so they sweeten long-term saving with tax relief or tax-free growth — provided you leave the money to do its job. Understanding that bargain is the key to using these accounts well.

Why Retirement Accounts Exist

Retirement accounts aren't an accident of the tax code — they're deliberate policy. People left to their own devices tend to under-save for a retirement that feels far away, and a population that reaches old age with no savings becomes a burden on the state. So governments use the most powerful lever they have — tax — to nudge behaviour: contribute to a recognised retirement account, and you get a tax advantage you can't get elsewhere.

That's why pensions carry benefits like tax relief on contributions (a boost going in) or tax-free growth, and why they restrict early access: the incentive is explicitly designed to keep the money saved until retirement. For you, the investor, this means retirement accounts offer a genuinely better deal than ordinary saving for money you won't need until later life — a tailwind the tax system hands you for doing the sensible thing anyway.

The Three Pillars Of Retirement Income

In the UK, retirement income typically rests on three pillars, and a sound plan considers all three together.

- The State Pension is the government-provided baseline, funded through National Insurance contributions over your working life. It's a valuable foundation, but for most people it is not enough on its own to fund a comfortable retirement — which is precisely why the other pillars matter.

- Workplace pensions come through your employer. In the UK, auto-enrolment means most employees are automatically signed up, and — crucially — the employer usually contributes too.

- Private provision is what you arrange yourself: a SIPP (SIPPs), an ISA (ISAs) used for retirement, or other savings. This is the pillar you control entirely.

A realistic retirement plan treats these as a stack: the State Pension as a floor, topped up by workplace and private saving to reach the income you actually want.

The Employer Match: Free Money

Within the workplace pillar lies what is often the single best deal in personal finance: the employer match. When you contribute to a workplace pension, your employer typically adds their own money on top — sometimes matching your contribution pound for pound up to a limit.

This is as close to free money as finance offers. If your employer matches your contribution, then putting in £100 instantly becomes £200 (before any tax relief or investment growth) — a guaranteed, immediate 100% "return" no investment can reliably promise. Not contributing enough to capture the full match is leaving guaranteed money on the table. This is why, in almost any sensible priority order, claiming the full employer match comes first — before paying down low-interest debt, before a SIPP, before an ISA. It is the highest-certainty return available to most people.

A Sensible Priority Order

With limited money, where should retirement contributions go first? A widely-sensible order, building on the financial order of operations from Financial Goals:

- Secure the basics — emergency fund, and clear high-interest debt (which compounds against you).

- Capture the full employer match — the guaranteed return you can't beat elsewhere.

- Use tax-advantaged wrappers — further pension contributions (for the relief and lock) and/or an ISA (for tax-free flexibility), matched to your goals.

- Invest beyond in a general account once tax-advantaged space is well used.

This isn't rigid — circumstances vary — but the logic is consistent: take the guaranteed, highest-value steps first (match, debt, safety net), then optimise. The biggest mistakes are skipping the employer match, or delaying retirement saving altogether.

Time Is The Retirement Saver's Superpower

Retirement is the goal with the longest horizon, which means compounding (see Compound Growth) has the most room to work — and starting early matters more here than almost anywhere. A pound invested for retirement at 25 has forty years to compound; the same pound at 45 has twenty. Because compounding back-loads its gains into the later years, the early starter often ends up with dramatically more, even with smaller total contributions. The practical message is simple and powerful: start contributing to retirement as early as you can, even modestly. Time, not income or cleverness, is the retirement saver's greatest asset — and it's the one thing you can never get back once spent.

How Much Do You Need?

A natural question is "how big does my retirement pot need to be?" There's no single answer — it depends on the income you want, when you retire, and your other pillars — but a few framing ideas help. First, think in terms of the income you'll want in retirement, then work back to the pot that could sustain it, remembering the State Pension and any workplace pension will cover part of it. Second, account for inflation: as Inflation showed, the income that feels comfortable today will cost considerably more in decades' time, so targets must be inflation-adjusted. Third, a common rule of thumb suggests a sustainable withdrawal of a modest percentage of your pot each year, which implies you need a pot many times your desired annual income from it — a sobering figure that underlines why starting early and capturing every match and tax break matters so much.

The exact numbers deserve their own detailed treatment (and, for big decisions, professional advice), but the qualitative lesson is clear: retirement is expensive precisely because it may last decades, so the combination of long-horizon compounding, tax advantages and employer contributions isn't a luxury — it's what makes the goal achievable at all.

Drawing Down In Retirement

Saving is only half the journey; eventually you draw the money out. While the detail is beyond this overview, it's worth knowing the broad shape. The State Pension pays a regular income for life. Workplace and private pensions can typically be accessed from a minimum age, often with a portion available tax-free and the rest taxed as income (see SIPPs). ISAs can be drawn tax-free at any time, which makes them a flexible complement for managing your taxable income in retirement — for instance, blending taxed pension withdrawals with tax-free ISA withdrawals.

The key idea is sustainability: a pot must last potentially decades, so withdrawals need to be paced so the money doesn't run out, while remaining partly invested to keep growing against inflation. The shift from accumulating to drawing down is a significant transition, and the accounts you built over a lifetime — and how they're taxed on the way out — shape the choices you'll have. Building across all three pillars gives you the most flexibility when that day comes.

Risks & Considerations

- Access is restricted. Pension money is locked until a minimum age — don't put money you need sooner into one.

- Market risk remains. Retirement accounts shelter tax, not market falls; the investments inside still rise and fall (though a long horizon helps).

- Rules change. Allowances, ages, relief and the State Pension are set by government and subject to change over your lifetime.

- The State Pension is rarely enough alone — relying on it without other pillars risks a difficult retirement.

- Don't leave the match unclaimed — perhaps the most common and costly retirement-saving error.

Common Misconceptions

- "The State Pension will be enough." For most, it's a foundation, not a full income — the other pillars are usually essential.

- "Retirement is too far away to start now." The early years are the most valuable for compounding; delay is the costliest mistake.

- "Pensions are too complicated to bother with." The core ideas — match, relief, start early — are simple and hugely impactful.

- "I should pick either a pension or an ISA." They're complementary; many people sensibly use both alongside any workplace pension.

Real-World Application

Picture someone in their twenties starting their first job, auto-enrolled into a workplace pension they barely notice. They're tempted to opt out to boost their take-home pay. Understanding retirement accounts changes that decision entirely: by staying in and contributing enough to get the full employer match, they capture an instant, guaranteed doubling of part of their contribution, plus tax relief, plus forty years of compounding. They then open an ISA for flexible long-term money and, later, perhaps a SIPP for extra pension saving. Decades on, those three pillars together — state, workplace and private — fund a comfortable retirement that would have been impossible on the State Pension alone. The single most important move was the earliest and easiest one: not opting out, and claiming the match. That is the everyday power of understanding retirement accounts.

Key Takeaways

- Retirement accounts are tax-advantaged pensions designed to reward long-term saving — tax incentives in exchange for restricted access.

- Retirement income rests on three pillars: the State Pension (foundation), workplace pensions, and private provision (SIPP/ISA).

- An employer match is free money — a guaranteed instant return; capturing it in full usually comes first.

- A sensible priority order: basics → employer match → tax-advantaged wrappers → beyond.

- Start early — retirement's long horizon makes compounding, and the timing of contributions, decisive.

- Pensions and ISAs are complementary; together with a workplace pension they form a complete plan.

Finished this lesson? Track your progress.

Frequently asked questions

What is the main bargain behind retirement accounts?

Retirement accounts offer tax incentives — such as tax relief on contributions or tax-free growth — in exchange for leaving your money invested until a minimum age. This bargain is designed to encourage long-term saving by giving you a tax advantage you can't get with ordinary savings accounts.

Why do governments create tax-advantaged retirement accounts?

Governments use tax incentives to encourage people to save for retirement because people naturally under-save for a retirement that feels distant. Without this nudge, populations reaching old age with insufficient savings would become a burden on the state, so governments sweeten long-term saving to align personal incentives with public benefit.

What are the three pillars of retirement income in the UK?

The three pillars are: the State Pension (a government-provided baseline funded through National Insurance), workplace pensions (often including employer contributions through auto-enrolment), and private provision (such as a SIPP or ISA that you control yourself). Together they form a stack, with the State Pension as a floor topped up by workplace and private saving.

Why is claiming an employer match considered free money?

An employer match is free money because when you contribute to a workplace pension, your employer typically adds their own money on top — often matching your contribution pound for pound up to a limit. This creates an instant, guaranteed return before any investment growth or tax relief, making it one of the highest-certainty returns available.

What is the recommended priority order for retirement contributions?

The sensible priority order is: first, secure an emergency fund and clear high-interest debt; second, capture the full employer match; third, use other tax-advantaged wrappers like additional pension contributions or an ISA; and fourth, invest beyond tax-advantaged space in a general account once tax-advantaged room is well used.

Key terms

Next lesson

Continue learning

Choosing A Broker

Related topics

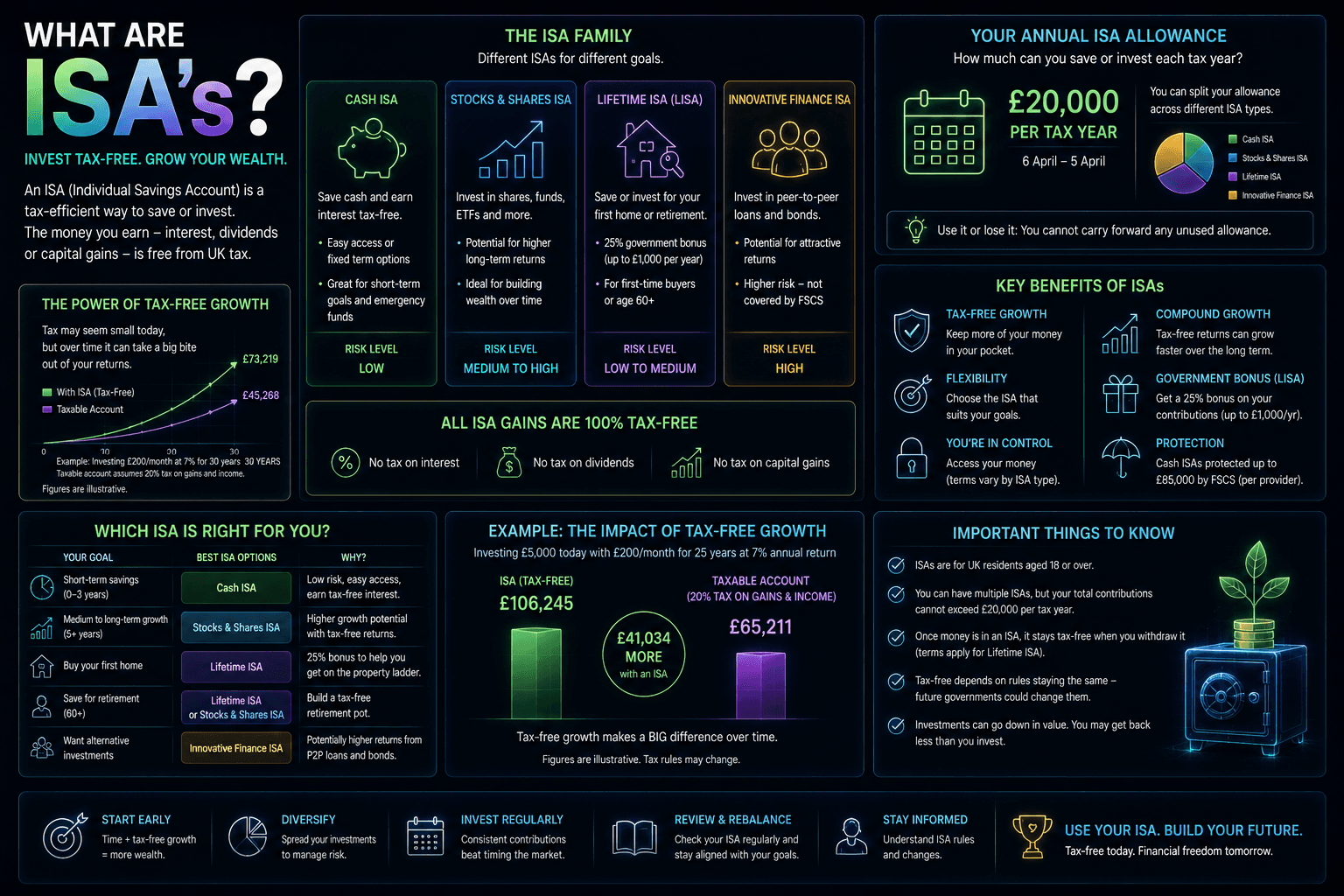

ISAs

The UK's tax-free wrapper for saving and investing: what an ISA is, the main types, the annual allowance, why tax-free growth and withdrawals matter so much over time, and how the Stocks & Shares ISA fits a long-term plan.

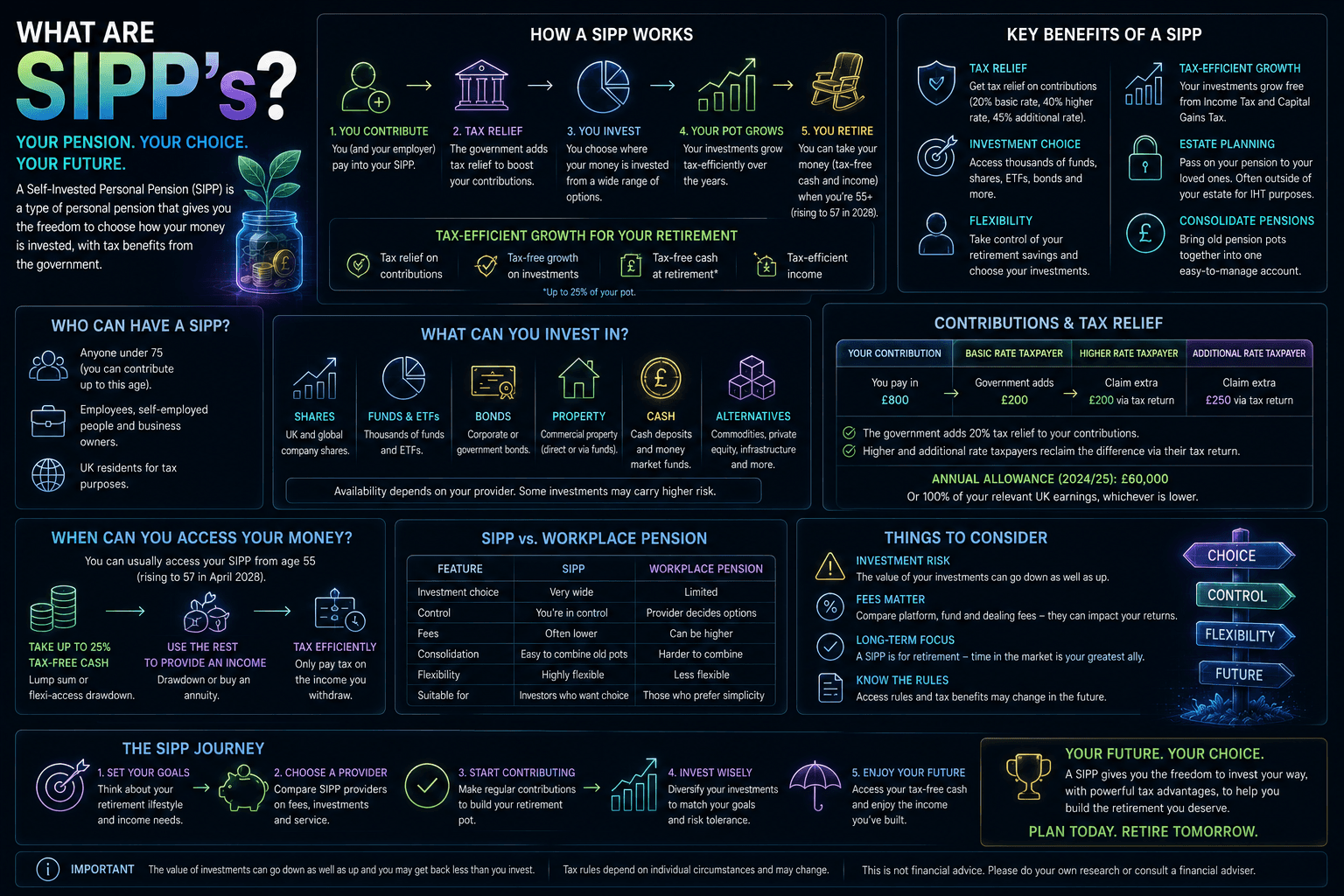

SIPPs

The UK's self-invested personal pension: how a SIPP works, the tax relief that boosts contributions, why the money is locked until a minimum age, how withdrawals are taxed, and how it compares with an ISA.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.