Commissions

The explicit cost of trading: what commissions are, the forms they take, how the spread and currency fees act as hidden commissions, why 'commission-free' isn't free, and how trading costs quietly erode returns.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 23 July 2026 · Editorial policy

Before this, read

Introduction

Every time you buy or sell an investment, there is a cost to making that transaction happen. Historically, the most visible form of that cost was the commission — a fee your broker charged to execute the trade. Commissions have fallen dramatically over the years, and many brokers now advertise "commission-free" trading. But as you'll see, the cost of trading never truly disappears; it merely changes form.

This lesson explains what commissions are, the different shapes they take, and the "hidden" commissions — the spread and currency fees — that you pay without ever seeing a fee line. It shows why trading costs matter so much more for small and frequent trades, why "free" isn't free, and how these costs quietly erode returns over time. It builds on What Is A Broker? and How Brokers Make Money, and pairs with What Is Payment For Order Flow?.

Quick Definition

A commission is the explicit fee a broker charges to execute a buy or sell order. More broadly, the cost of trading also includes implicit charges — chiefly the spread and currency-conversion fees — that are built into the price rather than itemised.

The key distinction is between explicit costs (a fee you can see and name) and implicit costs (a cost baked into the price you receive). A complete picture of what trading costs you must include both, because a broker can advertise zero explicit commission while charging plenty implicitly.

A Brief History: From Hundreds To Zero

To understand today's "free" trading, it helps to know where commissions came from. For most of the twentieth century, brokerage commissions were fixed — set by the exchanges themselves — and very high. Buying shares could cost the equivalent of a substantial sum in fees, which kept ordinary people out of the market and made frequent trading prohibitively expensive.

When fixed commissions were deregulated, brokers began competing on price, and the cost of a trade fell steadily for decades — from hundreds of dollars, to tens, to single digits, and finally, in the app era, to zero. This is a genuine good-news story: the collapse of commissions democratised investing. But each fall pushed brokers to find new ways to earn, which is why today's "commission-free" brokers lean so heavily on the implicit and behind-the-scenes streams. Seen in this light, zero commission is not a break from history but its logical endpoint: the visible fee driven all the way down, while the invisible costs quietly took up the slack. The history teaches the enduring lesson — always look past the headline number to the total cost.

The Forms A Commission Takes

When brokers do charge explicit commissions, they typically use one of a few structures:

- Flat fee per trade — a fixed amount regardless of trade size (e.g. $5 per trade). Simple, but a heavy burden on small trades.

- Per-share — a small charge for each share traded, common in some markets.

- Percentage of trade value — a percentage of the amount transacted, so larger trades cost more in absolute terms.

- Tiered — rates that fall as your trading volume rises, favouring active traders.

Each structure suits different investors. A flat fee rewards large, infrequent trades; a percentage fee can be gentler on small trades but costly on large ones. Knowing the structure tells you which trading patterns a broker's pricing favours.

The Hidden Commissions

Here is what catches many investors out: the most significant trading costs are often the ones that aren't called commissions at all.

- The spread. You generally buy at the higher ask price and sell at the lower bid price. That gap — the spread — is an implicit cost you pay on every round trip, whether or not a commission is charged. On liquid assets it's tiny; on illiquid ones it can dwarf any commission. (See What Is Market Structure?.)

- Currency-conversion (FX) fees. Buying foreign shares means converting currency, and brokers often add a markup of 0.5%–1.5% to the exchange rate. For an investor holding overseas shares, this is frequently the largest single trading cost — and it rarely appears as a "commission."

Because these are baked into the price, a "commission-free" broker can quietly earn more from a trade than a broker charging a small, transparent commission. The lesson: judge trading cost by the all-in total — commission plus spread plus FX — not the headline.

To see the spread as a real commission, work a quick example. Suppose a share has a bid of $99.90 and an ask of $100.10 — a 20p spread. You buy at $100.10 and, if you sold immediately, you'd receive only $99.90: you're instantly "down" 20p per share, or about 0.2%, purely from the spread, before the price moves at all. On a $10,000 position that's $20 on the way in and another $20 on the way out — $40 round-trip — with not a single "commission" charged. On a tight, liquid instrument the spread might be a penny or less (negligible), but on a thinly traded one it can be several percent. This is why two "commission-free" trades can have wildly different real costs, and why liquidity matters so much: the spread is a commission you pay to the market itself, and you minimise it by trading liquid assets.

Why "Commission-Free" Isn't Free

The collapse of commissions to zero was a genuine milestone that lowered barriers and brought millions into investing. But, as How Brokers Make Money explains, a broker is a business, and removing the visible commission simply relocates the cost. A "free" broker typically earns through the spread, payment for order flow, FX markups, interest on your idle cash, or premium subscriptions. The trade is "free" of an explicit commission, not free of cost.

This doesn't make commission-free trading a scam — for a buy-and-hold investor making occasional trades of liquid funds, the all-in cost can genuinely be very low. The point is simply to stay clear-eyed: "free" is a marketing label about one cost line, not a statement about your total cost. Always ask what fills the gap where the commission used to be.

Why Commissions Hurt Small And Frequent Trades Most

Trading costs are not felt equally. They fall hardest on two groups: those trading small amounts and those trading frequently.

A $5 flat fee is a painful 5% of a $100 trade — your investment must rise 5% just to break even — but a trivial 0.05% of a $10,000 trade. So small trades are disproportionately burdened by any fixed cost. And because every trade incurs the cost, frequency multiplies it: trade twenty times a year and you pay the cost twenty times. This is the arithmetic behind a core principle of long-term investing: trade infrequently, in larger amounts. Fewer, bigger trades spread fixed costs thinly and avoid repeated charges, while frequent small trades hand a steady stream of your capital to costs.

How Costs Erode Returns Over Time

Trading costs don't just nibble at a single trade — they compound against you over a lifetime, exactly as returns compound for you. Every dollar paid in commissions, spreads and fees is a dollar that never gets to grow.

As shown in Compound Growth, even a difference of a fraction of a percent a year can consume a large slice of your final wealth over decades. Consider an investor with $50,000 who, through frequent small trades, loses 1.5% a year to combined costs while a disciplined peer loses just 0.2%. That 1.3% annual gap, on a portfolio growing at 7%, compounds into tens of thousands of dollars of forgone wealth over thirty years — not from bad luck or poor stock-picking, but purely from the friction of transacting too much, too expensively. This is why minimising costs is one of the few levers in investing that is entirely within your control and reliably pays off, year after year.

Beyond Commissions: Other Costs To Know

A complete picture of trading costs includes a few more items that aren't commissions but hit your returns all the same:

- Taxes and duties. Some markets levy a transaction tax — for example, UK Stamp Duty Reserve Tax of 0.5% on most UK share purchases. This is paid to the government, not the broker, but it's a real cost of the trade, so factor it in (note that many ETFs and some other instruments are exempt).

- Exchange and regulatory fees. Tiny per-trade levies that brokers sometimes pass through. Usually negligible for ordinary investors, but they exist.

- Platform / account fees. Separate from per-trade commissions, some brokers charge an ongoing fee to hold an account or use the platform — sometimes a flat amount, sometimes a percentage of assets. Over time these recurring fees can outweigh per-trade costs, especially for buy-and-hold investors who rarely trade.

- Fund charges. If you buy funds, their own expense ratios are a separate, ongoing cost layered on top of any trading cost (see What Is An ETF?).

The takeaway is that "cost of investing" is broader than "commission." A truly low-cost setup minimises the whole stack: trading costs, spreads, FX, platform fees, taxes where avoidable, and fund charges. Optimising one while ignoring the others can leave you paying more than you think.

Minimising Your Trading Costs

The practical defences follow directly from everything above:

- Trade less. For long-term investing, infrequent trading is both cheaper and usually better for returns.

- Trade in larger amounts. Consolidating contributions into fewer, larger purchases spreads any fixed cost thinly.

- Mind the spread. Favour liquid assets (broad funds, large companies) with tight spreads; be cautious with illiquid ones.

- Watch FX fees. If you hold foreign shares, the currency markup may be your biggest cost — compare brokers on it specifically.

- Compare all-in cost, not headlines. Add commission + spread + FX + platform fees for your trading pattern, and choose accordingly.

Common Misconceptions

- "Commission-free means free." It relocates the cost to spreads, FX, order flow or interest on cash.

- "Commissions are the only trading cost." The spread and FX fees are often larger, and entirely real.

- "Small trades are cheap because the fee is small." A small fee can be a huge percentage of a small trade — costs are about proportion, not absolute size.

- "Costs are too small to matter." Compounded over decades, recurring costs can consume a large share of returns.

Real-World Application

Imagine an investor who likes to "top up" with $100 every week into a US share through a "commission-free" app. It feels free — there's no commission line. But each purchase crosses a small spread and incurs a ~1% currency-conversion fee, so roughly $1+ of every $100 is lost to costs, week after week — over $50 a year on $5,200 invested, plus the spread drag, all invisible. A second investor instead invests $1,300 once a quarter into a low-cost, broad fund in their own currency, paying a tiny spread and no FX fee. Same money invested, but the second investor keeps far more of it working — simply by trading less often, in larger amounts, in cheaper instruments. Understanding commissions and their hidden cousins is what turns "it feels free" into a genuinely low-cost reality.

Key Takeaways

- A commission is the explicit fee to execute a trade; the spread and FX fees are implicit "hidden" commissions baked into the price.

- "Commission-free" isn't free — the cost is relocated to spreads, order flow, FX or interest on cash; judge the all-in cost.

- Fixed costs hit small and frequent trades hardest, because the fee is a larger percentage and is paid repeatedly.

- Trading costs compound against you over time, quietly eroding long-term returns.

- Minimise them by trading less, in larger amounts, in liquid instruments, and choosing a broker with low all-in costs for your style.

Finished this lesson? Track your progress.

Frequently asked questions

What is a commission in trading?

A commission is the explicit fee a broker charges to execute a buy or sell order. It is a visible, named cost separate from other trading expenses like the spread and currency-conversion fees.

What are the hidden costs of trading besides commissions?

The main hidden costs are the spread (the gap between the buy and sell price you receive) and currency-conversion fees (a markup of 0.5%–1.5% that brokers add when you buy foreign shares). These costs are baked into the price you pay rather than shown as a separate fee.

Why is 'commission-free' trading not actually free?

A broker advertising zero commission still earns money through implicit costs like the spread and currency-conversion fees, which are hidden in the price rather than itemized. The total cost of trading includes explicit commission plus these invisible charges, so a "free" broker can still charge significantly through these other means.

How do different commission structures work?

Brokers may charge a flat fee per trade, a per-share fee, a percentage of the trade value, or tiered rates that fall with higher trading volume. Each structure favors different trading patterns—for example, a flat fee benefits large infrequent trades, while a percentage fee can be gentler on small trades.

Why does the spread act like a hidden commission?

When you buy a share, you pay the higher ask price, and when you sell, you receive the lower bid price. That gap is an implicit cost paid on every trade; on a round trip with a 20p spread on a $100 share, you lose about 0.2% before the price even moves, making it a real cost even without an explicit commission charge.

Key terms

Next lesson

Continue learning

Cash Accounts

Related topics

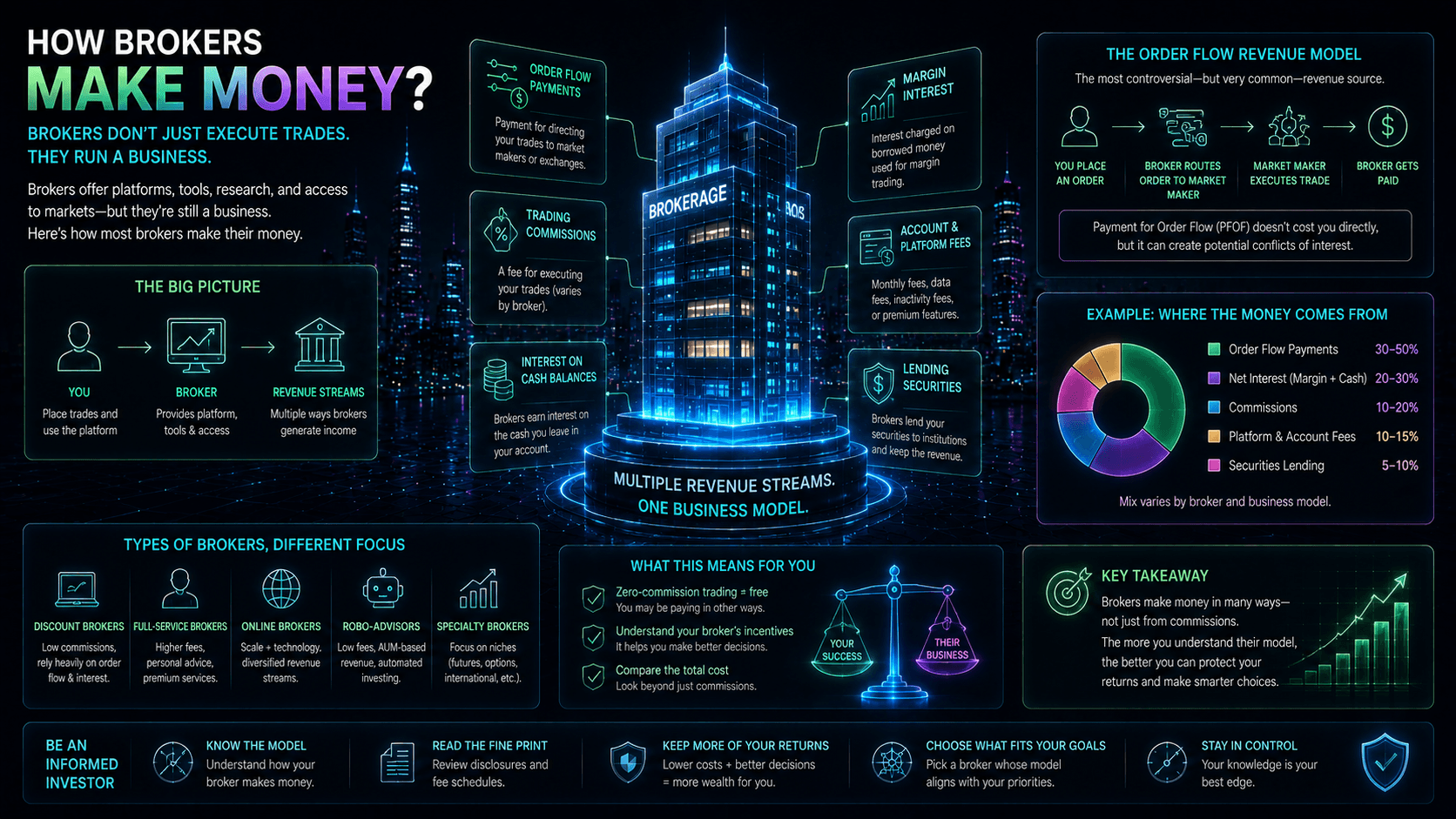

How Brokers Make Money

A complete map of every way a broker earns — commissions, spreads, payment for order flow, margin interest, interest on your cash, securities lending, FX and fees — and which revenue streams align with your interests and which work against them.

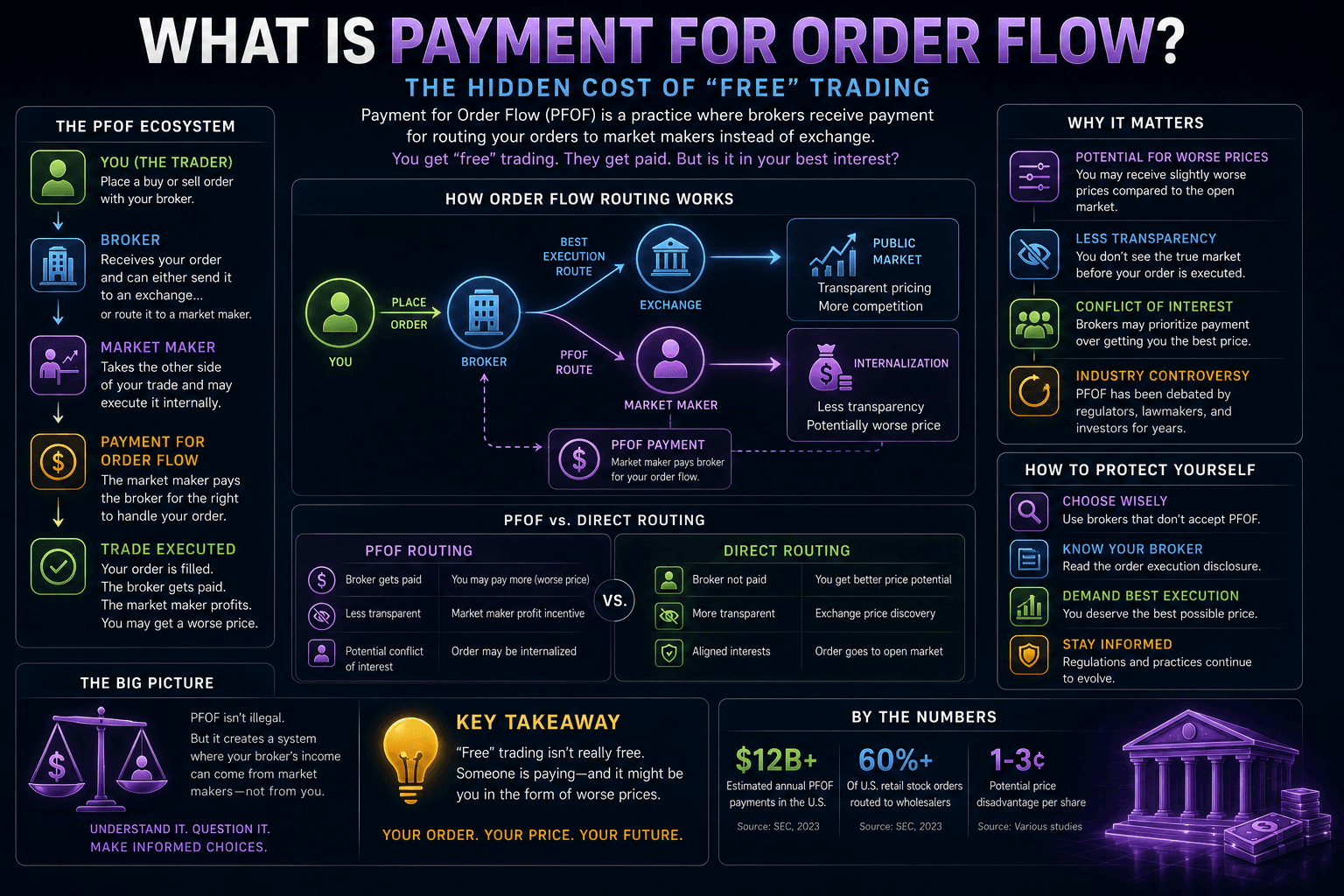

What Is Payment For Order Flow?

A balanced explanation of payment for order flow: how it funds commission-free trading, why market makers pay for retail orders, the conflict of interest it creates, price improvement and the NBBO, and what it means for you.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.