How Brokers Make Money

A complete map of every way a broker earns — commissions, spreads, payment for order flow, margin interest, interest on your cash, securities lending, FX and fees — and which revenue streams align with your interests and which work against them.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 23 July 2026 · Editorial policy

Before this, read

Introduction

You've learned what a broker is and the essential service it provides. Now comes a question that reveals a great deal about the modern investing landscape: how does a broker actually make money — especially one that proudly charges "zero commission"? The answer is not a single fee but a surprisingly rich menu of revenue streams, some obvious and some all but invisible.

This matters far more than idle curiosity. A broker's revenue model shapes its incentives, and those incentives quietly affect the prices you get, the costs you pay, and even how often you're nudged to trade. This lesson maps every major way brokers earn, explains which streams align with your interests and which work against them, and gives you a simple, powerful habit — follow the money — for evaluating any broker. It builds on What Is A Broker? and connects to the deeper dives on Commissions and Payment For Order Flow.

Quick Definition

Brokers earn money through a mix of explicit charges (commissions, fees) and less visible streams (spreads, payment for order flow, interest on cash, margin interest, securities lending, currency conversion). "Free" trading simply shifts the cost from the visible column to the invisible one.

The single most important idea is this: a broker is a business, and a business must generate revenue. When you can't see how it earns, that doesn't mean it earns nothing — it means the revenue is coming from somewhere you're not looking. Learning where to look is the whole point of this lesson.

Why It Matters To You

It's tempting to think a broker's business model is its concern, not yours. But because the model determines the broker's incentives, it directly affects you in three ways: the price you receive on trades, the total cost you bear (visible and hidden), and the behaviour the broker encourages. A broker that earns per trade has an incentive to make you trade more; one that earns from your idle cash has little incentive to help you invest it; one paid by a third party to route your orders may not route them purely for your benefit. None of this makes brokers villains — most are legitimate, regulated businesses — but understanding their incentives lets you choose wisely and see the true cost behind the marketing.

The Full Menu Of Revenue Streams

Brokers draw on some or all of the following. Knowing each by name lets you recognise it in any broker's fine print.

Let's walk through each less-obvious stream, since these are the ones that catch investors out:

- The spread. Some brokers quote you a slightly worse price than the true market price and keep the difference. It never appears as a "fee," but it's a real cost embedded in every trade. (Covered in depth in Commissions and What Is Market Structure?.)

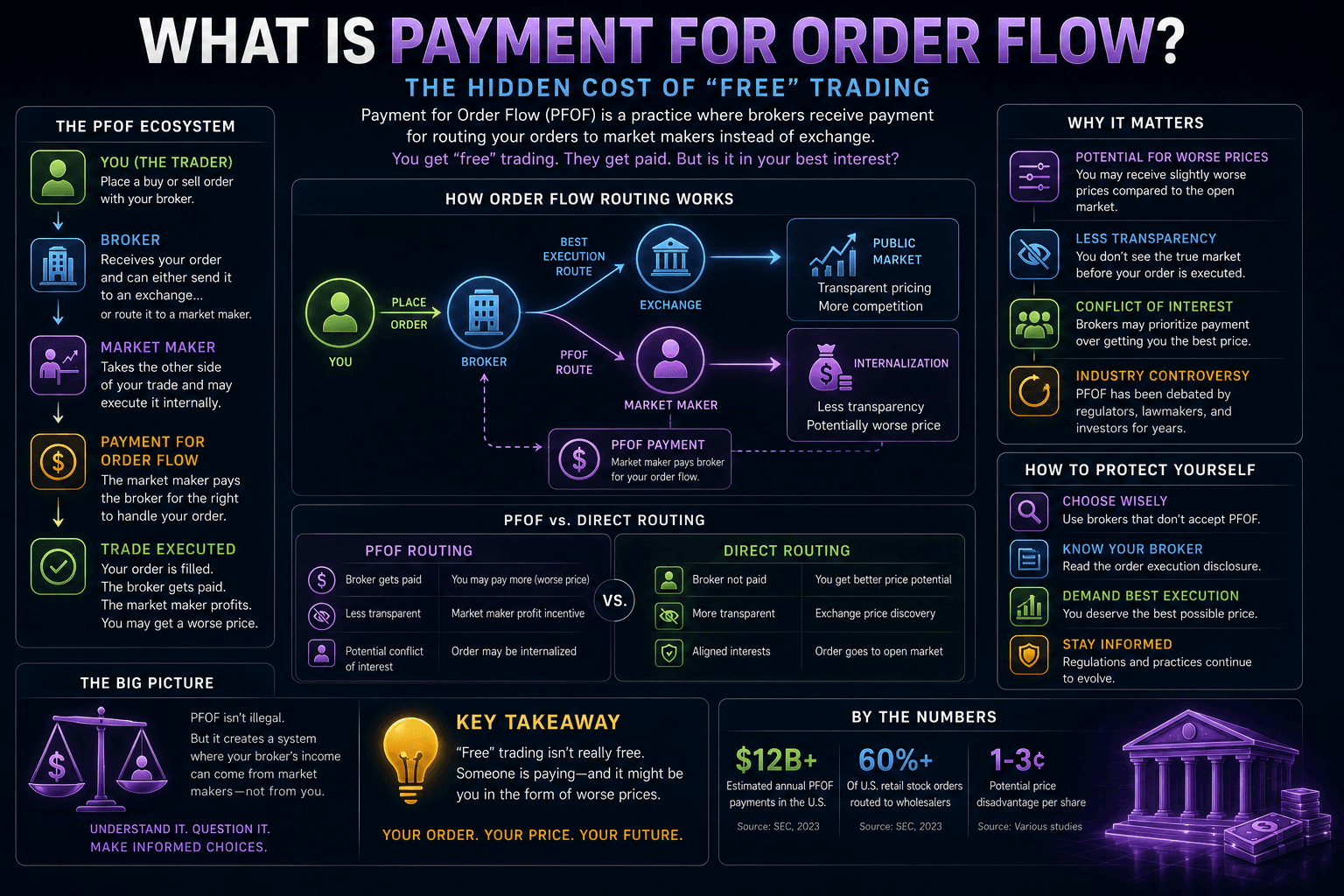

- Payment for order flow (PFOF). Instead of charging you, the broker sells the right to execute your orders to large trading firms, which pay for the steady stream of retail orders. This funds much "free" trading and is significant enough to warrant its own lesson.

- Interest on idle cash. The uninvested cash in your account earns the broker interest (it places that cash in safe, interest-bearing instruments). Brokers often keep most or all of this — a huge, quiet revenue source, particularly when interest rates are high.

- Margin interest. Brokers lend customers money to buy more than their cash allows and charge interest on those loans. (See Margin Accounts.)

- Securities lending. Brokers can lend out the shares held in client accounts to other market participants — for example, short sellers — and earn a fee, sometimes sharing a slice with the customer.

The visible charges — commissions, platform fees, FX and withdrawal fees — are easier to spot but no less real. Notice that currency-conversion fees on foreign shares are frequently larger than any commission ever was.

The Economics Of "Free"

The rise of commission-free trading is the clearest illustration of how this works. For decades, the commission was the obvious, visible cost. When brokers competed it down to zero, the cost did not vanish — it relocated to the less-visible streams.

This isn't necessarily sinister — commission-free trading genuinely lowered barriers and often delivers fine value, especially for buy-and-hold investors. But it means the honest question is never "what's the commission?" It's "how does this broker actually make money from me, and how much?" A broker earning mainly from interest on your cash and a small FX fee may be cheaper for you than a "free" one earning from wide spreads and aggressive order-flow deals — or vice versa. You can only tell by looking past the headline.

Aligned vs Misaligned Incentives

Here is the framework that turns this knowledge into judgement. Revenue streams differ in how well their incentives align with your interests as an investor.

A transparent flat fee (say, a fixed monthly platform charge or a clearly disclosed commission) is comparatively well aligned: it doesn't rise when you trade more or get a worse price, so the broker profits whether or not you churn your account. Streams that profit from your activity (per-trade revenue, which rewards encouraging overtrading), your inertia (keeping the interest on cash you forgot to invest), or worse execution (wide spreads, certain order-flow arrangements) pull against your interests, even when entirely legal and disclosed. This doesn't mean a broker using them is bad — most use a mix — but it tells you where to be alert. A broker whose profit depends on you doing the wrong thing for your wealth deserves more scrutiny than one whose profit is indifferent to your behaviour.

Different Broker Models Earn Differently

The revenue mix isn't random — it tends to follow the type of broker, which helps you anticipate where a given firm makes its money.

A full-service broker, offering advice and a personal relationship, typically earns through higher, transparent fees — commissions, a percentage of assets managed, or advice charges. The cost is visible and high, but the incentive is relatively clear: you're paying for service. A discount or execution-only broker competes on low headline cost, so it leans more on the less-visible streams — spreads, interest on cash, FX fees, and, where permitted, order-flow payments. A robo-advisor usually charges a small, transparent annual percentage of your portfolio to build and manage it automatically — a model whose incentive (grow your portfolio, since its fee scales with it) is reasonably aligned, though you still pay every year.

The flashy, "free" trading apps that have drawn in so many new investors generally sit at the discount end, monetising heavily through order flow, spreads, FX, interest on cash, and premium subscription tiers. None of these models is inherently good or bad — but knowing the type of broker tells you, before you even read the fine print, roughly where to look for the cost and what incentive is driving it.

The Engagement Incentive

One revenue dynamic deserves special caution because it can quietly harm you: the incentive to maximise your engagement. When a broker earns more the more you trade — through per-trade revenue, spreads or order flow — its commercial interest is to get you trading as often as possible. This is why some apps feel like games: push notifications about price moves, celebratory animations on trades, streaks, leaderboards, and easy access to risky products. These features are not designed to make you a better investor; they're designed to increase activity, because activity is revenue.

For a long-term investor, this is precisely backwards. As covered in Investing vs Trading, frequent trading usually erodes returns through costs and mistakes — so a design that maximises the broker's engagement revenue can directly undermine your wealth. The defence is awareness: recognise gamified nudges for what they are, and remember that with long-term investing, less activity is usually better. A broker whose business model rewards your overtrading is one to use deliberately and sparingly, never on its own terms. The healthiest relationship with such a platform is often a boring one.

A Worked Example

Imagine a "free" broker and a typical buy-and-hold investor with $10,000, of which $1,000 sits as uninvested cash, who makes a few foreign-share purchases a year. The broker shows $0 in commissions — but it might earn: a slice of the spread or an order-flow payment on each trade; the interest on that $1,000 of idle cash (perhaps $40–50 a year at higher rates, largely kept); and a 0.5%–1.5% currency-conversion fee on the foreign purchases. None of this appears as a "fee" on the statement, yet it can add up to more than a transparent broker's modest commission would have cost. The investor feels like they're paying nothing, while quietly contributing through several channels at once. Seeing this clearly is what lets you compare brokers on their true, all-in cost rather than their marketing.

How To Find Out What Your Broker Earns

You don't need to be an analyst to follow the money. A few checks reveal most of it:

- Read the fee schedule and key information documents — brokers must disclose their charges, including FX rates, platform fees and (where applicable) order-flow practices.

- Check what interest you receive on cash versus the prevailing rate — the gap is the broker's cut.

- Compare the buy and sell prices quoted on something you'd trade to gauge the spread.

- Note the currency-conversion fee if you'll hold foreign shares — often the biggest hidden cost.

- Check the jurisdiction — some practices (like PFOF) are restricted in places like the UK and EU, which changes the revenue mix.

The goal isn't to find a broker that earns nothing from you — that can't exist — but to understand how it earns and judge whether that's fair and competitive for the way you invest.

Risks & Considerations

- "Free" can cost more. Hidden streams sometimes exceed what a transparent fee would have been; always compare total cost.

- Incentives can work against you. Per-trade and engagement-based revenue can encourage overtrading, which harms long-term returns.

- Idle cash is quietly monetised. Large uninvested balances earn the broker, not you — a reason not to leave money lying idle.

- Securities lending and order routing happen behind the scenes; reputable, regulated brokers manage these with safeguards, but they're worth understanding.

Common Misconceptions

- "Zero commission means free." It means the cost moved to less visible streams.

- "All brokers make money the same way." Revenue mixes vary enormously, and so do their incentives and total costs.

- "If I can't see a fee, I'm not paying one." Spreads, FX charges and forgone interest are real costs you simply can't see on a statement.

- "How my broker earns is none of my business." Its model shapes its incentives, which shape your prices, costs and the behaviour it encourages.

Real-World Application

Two investors compare brokers. The first picks purely on "zero commission" and never looks further. The second spends ten minutes following the money: they find Broker A earns mainly from a transparent platform fee and passes on most cash interest, while Broker B is "free" but earns from wide FX margins and keeps all the interest on idle cash. For the second investor — who holds some foreign shares and a cash buffer — Broker A is meaningfully cheaper and its incentives are better aligned, despite the visible fee. Same market, same goals, but understanding how brokers earn led to a genuinely better, cheaper choice. That is the practical payoff of following the money.

Key Takeaways

- Brokers earn through visible charges (commissions, platform, FX, withdrawal fees) and less-visible streams (spreads, PFOF, interest on cash, margin interest, securities lending).

- "Free" trading relocates cost rather than removing it — always ask how a broker actually earns from you.

- Revenue streams differ in incentive alignment: transparent fees align better; activity-, inertia- and worse-execution-based revenue can pull against you.

- Idle cash is a major quiet revenue source — don't leave money lying uninvested by accident.

- Follow the money: read the fee schedule, check cash interest, spreads and FX fees, and judge the true all-in cost — not the headline.

Finished this lesson? Track your progress.

Frequently asked questions

What are the main ways brokers make money besides commissions?

Brokers earn through spreads (marking up prices), payment for order flow (selling your order execution rights to trading firms), interest on your idle cash, margin interest (lending you money), and securities lending (loaning your shares to other market participants). These less-visible streams often grow larger when commissions are eliminated.

Why do brokers offer commission-free trading if they need to make money?

Commission-free trading doesn't eliminate broker revenue—it relocates it to less-visible streams like spreads, payment for order flow, interest on cash, and FX fees. The cost doesn't vanish; it simply moves from an obvious line item to hidden charges embedded in your trades and account.

How does a broker's revenue model affect the prices I get when trading?

A broker's revenue model shapes its incentives, which directly affect the prices you receive on trades, your total costs (visible and hidden), and the trading behavior the broker encourages. For example, a broker earning mainly from spreads has an incentive to widen them, while one paid per trade has an incentive to encourage more trading.

What is payment for order flow and how does it affect me?

Payment for order flow occurs when brokers sell the right to execute your orders to large trading firms, which pay for the steady stream of retail orders. This revenue stream funds much of the "free" trading offered today and is significant enough that understanding it helps explain your true trading costs.

Is a broker earning from my idle cash aligned with my interests?

A broker that earns interest on your uninvested cash has little incentive to help you invest it, creating a misaligned incentive. This is a particularly large, quiet revenue source when interest rates are high, meaning the broker may benefit from you keeping money sitting idle rather than deployed in investments.

Key terms

Next lesson

Continue learning

Commissions

Related topics

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.