Roth IRA

The US retirement account funded with after-tax money that then grows and pays out completely tax-free: how a Roth IRA works, the income limits, why contributions stay accessible, the absence of required withdrawals, and how to think about the Roth-versus-Traditional decision.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 23 July 2026 · Editorial policy

Before this, read

Introduction

Most retirement accounts give you a tax break now and tax you later. The Roth IRA flips that deal: you pay the tax up front, and in exchange, everything afterward — decades of growth and every qualified withdrawal in retirement — is completely tax-free. For many savers, especially earlier in their careers, that trade is extraordinarily valuable. The Roth IRA is, in spirit, the US cousin of the UK's tax-free wrapper: pay in from taxed income, then never pay tax on the growth again.

This lesson explains how a Roth IRA works, the income limits on contributing, why your contributions stay accessible, the absence of required withdrawals, and — most importantly — how to think about the Roth-versus-Traditional decision that sits at the heart of US retirement planning. (Tax rules are US-specific and can change; this is education, not tax advice.)

Quick Definition

A Roth IRA is an individual US retirement account funded with after-tax money. There's no deduction when you contribute, but qualified withdrawals in retirement — including all investment growth — are completely tax-free.

The Roth's defining feature is where the tax break lands: not on the way in, but on the way out. You give up the up-front deduction in exchange for never being taxed on the gains — and over a lifetime of compounding, those gains can dwarf the original contributions.

How A Roth IRA Works

You open a Roth IRA yourself at a broker, contribute money you've already paid income tax on (up to the annual limit), and invest it — typically in low-cost, diversified funds (see What Is An ETF?). From then on, the account grows with no tax on dividends, interest, or capital gains. And when you take qualified withdrawals in retirement, you owe nothing — not on your contributions, and not on a lifetime of growth.

Compare the two stages against a Traditional account:

- Going in — no deduction. You contribute after-tax dollars, so there's no tax break this year.

- Coming out — no tax. Qualified withdrawals, including all earnings, are entirely tax-free.

Income Limits

The Roth IRA's main gatekeeper is income. The ability to contribute directly to a Roth IRA phases out above certain income levels — as your income rises through a band, the amount you're allowed to contribute shrinks, and above the top of the band you can't contribute directly at all. The thresholds are set by the IRS and adjusted over time, so check the current figures.

(Higher earners sometimes use a legal workaround often called a "backdoor" Roth contribution; the mechanics are beyond this beginner lesson, but it's worth knowing the option exists.) The annual contribution limit itself is shared with the Traditional IRA — the cap applies across all your IRAs combined, not per account.

Accessible Contributions

The Roth IRA has a feature no other retirement account shares: because your contributions were already taxed, you can generally withdraw them — the amounts you put in, though not the earnings — at any time, tax- and penalty-free.

This makes the Roth unusually flexible — it can quietly double as an emergency backstop of last resort — though the intention should always be to leave it invested, because the real prize is decades of tax-free compounding on the earnings. Touch only the contributions, and only if you truly must.

No Required Minimum Distributions

There's one more Roth advantage worth highlighting: a Roth IRA has no Required Minimum Distributions during the original owner's lifetime. Traditional accounts force you to start drawing the money down (and paying the deferred tax) at a set age. A Roth doesn't — you can let it keep growing tax-free for as long as you like, which makes it a powerful tool for long-term and estate planning.

The Roth vs Traditional Decision

The central question is simple to state: pay tax now, or pay tax later? It hinges on whether you expect your tax rate to be higher or lower in retirement than it is today.

- Roth (pay tax now) tends to favor those who expect to be in a higher bracket later — classically, younger or early-career savers whose income (and tax rate) will likely rise. Lock in today's lower rate; withdraw tax-free at tomorrow's higher one.

- Traditional (pay tax later) tends to favor those who expect a lower bracket in retirement — often higher earners in their peak years who value the deduction now and anticipate a lower rate when they draw the money.

No one can predict future tax rates with certainty, which is why many people deliberately hold both — "tax diversification," giving flexibility to choose which account to draw from in any given retirement year. And remember the order of operations from 401(k): capture the full employer match first, then fund an IRA — Roth or Traditional — according to this decision.

Risks & Considerations

- It shelters tax, not market risk. Investments inside a Roth still rise and fall; tax-free growth doesn't prevent losses.

- No up-front break. You forgo a deduction today; the payoff is entirely in the future.

- Income limits apply. Higher earners may be unable to contribute directly.

- Earnings are locked. Only contributions are freely accessible; withdrawing earnings early can trigger tax and a penalty.

- Rules can change. Income limits, contribution caps and qualification rules are set by law and can be altered; check current figures.

Common Misconceptions

- "Roth withdrawals are taxed like other retirement accounts." Qualified Roth withdrawals — including all growth — are tax-free.

- "My Roth money is completely locked until retirement." Your contributions can generally be withdrawn anytime tax-free; only the earnings are restricted.

- "Roth is always better than Traditional." It depends on your current versus future tax rate — neither is universally superior.

- "High earners can't use a Roth at all." Direct contributions phase out with income, but other routes (like a backdoor Roth) can exist.

Real-World Application

Consider an early-career worker in a modest tax bracket who, after capturing their full 401(k) match, opens a Roth IRA and contributes the annual maximum into a broad index fund. They get no deduction today — but their bracket is low, so the tax cost is small. Over the next thirty or forty years, the account compounds tax-free, and because they expect to retire in a higher bracket, every dollar they eventually withdraw escapes tax that a Traditional account would have owed. Along the way, the knowledge that their contributions remain accessible gives peace of mind, even though they never touch them. They paid a little tax early to avoid a lot of tax later — the essence of the Roth, and for many savers, one of the best deals the US tax code offers.

Key Takeaways

- A Roth IRA is funded with after-tax money: no deduction now, but tax-free qualified withdrawals — including all growth — later.

- It's the "pay tax now" mirror of the Traditional account's "pay tax later," and resembles a tax-free investing wrapper.

- Income limits phase out direct contributions at higher earnings; the annual cap is shared across all your IRAs.

- Your contributions stay accessible anytime tax- and penalty-free; the earnings are locked until retirement age.

- A Roth IRA has no Required Minimum Distributions for the original owner — it can compound tax-free indefinitely.

- The Roth-vs-Traditional choice turns on whether your tax rate will be higher (favor Roth) or lower (favor Traditional) in retirement — and many people hold both.

Finished this lesson? Track your progress.

Frequently asked questions

What is a Roth IRA and how does it differ from a Traditional IRA?

A Roth IRA is a US retirement account funded with after-tax money that grows and pays out completely tax-free in retirement. Unlike a Traditional IRA, which gives you a tax deduction when you contribute but taxes you on withdrawals later, the Roth charges you tax upfront but then never taxes you again — not on the growth, and not on qualified withdrawals in retirement.

Can I withdraw my Roth IRA contributions before retirement?

Yes. Because your contributions were already taxed, you can withdraw the amounts you put in — though not the earnings — at any time without tax or penalty. However, the earnings portion remains locked until retirement age to preserve their tax-free status.

Who should choose a Roth IRA over a Traditional IRA?

A Roth IRA tends to favor those who expect to be in a higher tax bracket in retirement than they are today, especially younger or early-career savers whose income and tax rate will likely rise. By paying tax now at a lower rate and withdrawing tax-free later at a higher rate, you lock in a tax advantage.

Are there income limits for contributing to a Roth IRA?

Yes. The ability to contribute directly to a Roth IRA phases out above certain IRS income thresholds; as income rises through that band, your allowed contribution shrinks, and above the top you cannot contribute directly. These thresholds are adjusted over time, so current figures should be verified with the IRS.

Do I have to withdraw money from my Roth IRA at a certain age?

No. A Roth IRA has no Required Minimum Distributions during the original owner's lifetime, so you can let it keep growing tax-free for as long as you like, which makes it a powerful tool for long-term and estate planning.

Key terms

Next lesson

Continue learning

Choosing A Broker

Related topics

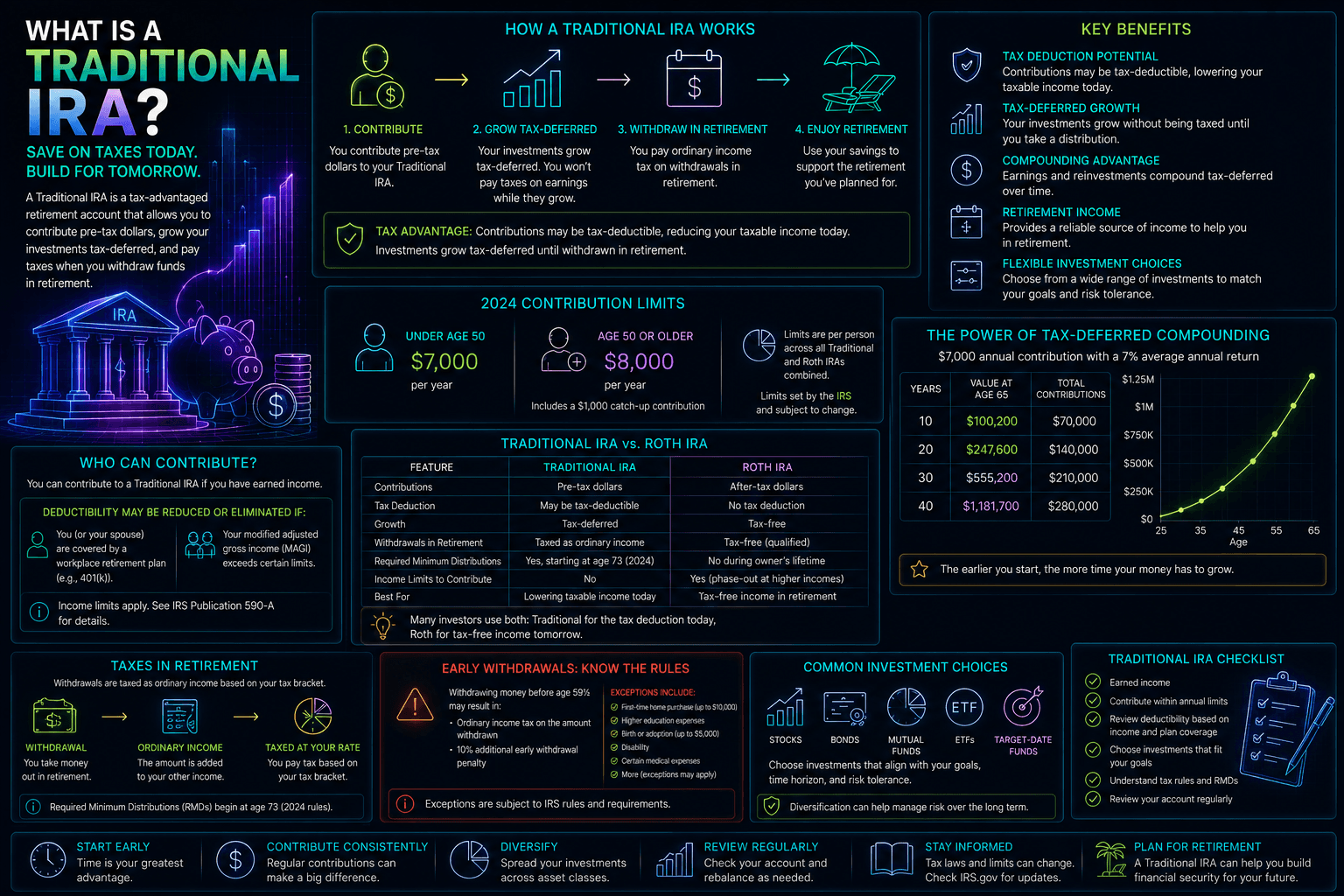

Traditional IRA

The individual US retirement account you open yourself: how Traditional IRA contributions can be tax-deductible, how tax-deferred growth compounds, how it differs from a 401(k), the annual limit, and the rules on deductibility, early access and required withdrawals.

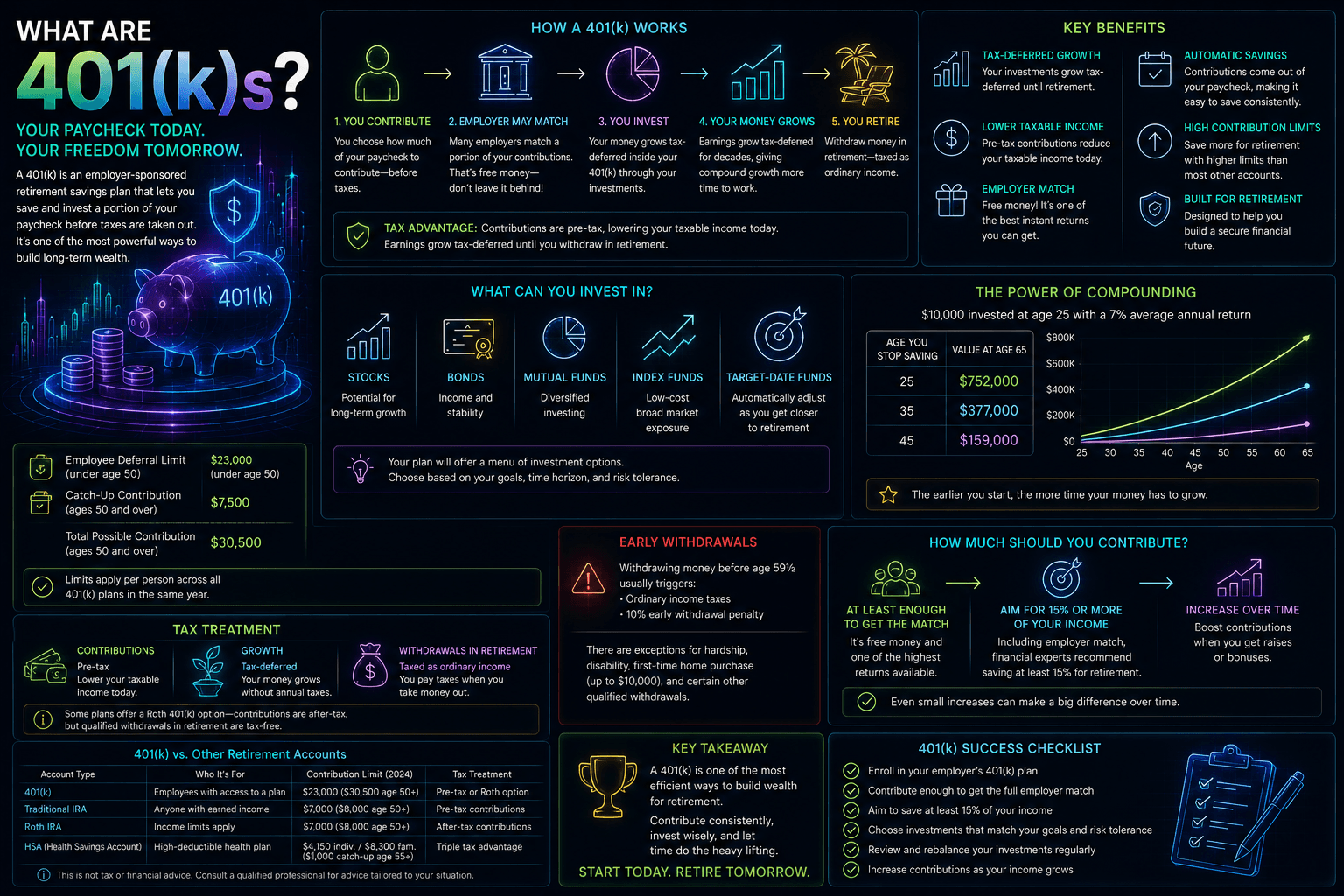

401(k)

The US workplace retirement plan: what a 401(k) is, how pre-tax (and Roth) contributions work, why an employer match is free money to claim first, how tax-deferred growth compounds, contribution limits, vesting, and the rules around accessing the money.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.